How GASB 75 Measures Implicit Cost in OPEB

Bottom Line Up Front

- Even when retirees appear to pay the “full premium,” governments may still be providing a hidden OPEB subsidy through blended healthcare rates.

- GASB 75 and ASOP 6 require actuaries to measure retiree healthcare costs using age-adjusted claims closets rather than blended premiums, which can significantly increase reported OPEB liabilities.

- Ignoring implicit cost can materially understate a government’s OPEB liability, annual expense, and long-term financial obligation, creating audit, funding, and credit rating risks.

When an employer provides retiree health benefits, the actual cost of those benefits typically varies by age. Older retirees generally use more healthcare and cost more to cover. If the employer charges all retirees (and often active employees) the same “blended” premium regardless of age, something subtle happens: the younger, healthier members of the group are subsidizing the older, higher-cost members.

Under Governmental Accounting Standards Board Statement No. 75 (GASB 75), and the actuarial guidance in ASOP 6, this subsidy is not considered free. It has a real economic cost to the employer that must be measured and disclosed. That hidden cost is known as the implicit rate subsidy, often referred to simply as the implicit cost.

What is the Implicit Rate Subsidy?

Here’s how it works in practice.

The actuary calculates what it would charge each age group if they were priced separately using age-adjusted or experience-rate costs. For example, a 62-year-old retiree might actually cost $1,800 per month to insure. However, the employer may only charge the retiree the same blended premium charged to everyone else – let’s say $900 per month.

The retiree is therefore paying far less than their actual cost. The employer is absorbing the difference, even if it never writes a check to the retiree directly. GASB 75 requires actuaries to recognize this gap as part of the OPEB liability.

ASOP 6 reinforces this by directing actuaries to use age-adjusted costs when projecting future benefits, rather than simply projecting the blended rate. This ensures that the subsidy embedded within the premium structure is not overlooked.

For a broader overview of implicit subsidies in OPEB plans, read our article here: Implicit Subsidies in OPEB Plans

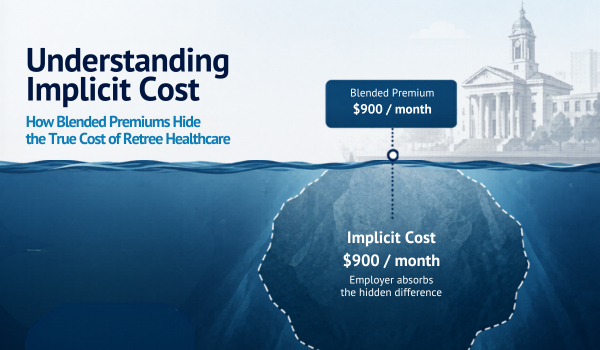

A Simple Illustration

The graphic below shows how an employer can be providing a significant OPEB subsidy even if it believes retirees are paying “the going rate”.

The active employee overpays relative to their age-adjusted cost, while the retiree underpays relative to theirs. The employer silently absorbs the gap between the two. That gap is the implicit cost, and both GASB 75 and ASOP 6 require it to be measured and

disclosed rather than buried in the blended premium.

How GASB 75 Measures the Implicit Cost

GASB 75 measures the implicit costs through a specific actuarial process. At its core, the standard requires OPEB liabilities to be measured using the “entry age” actuarial cost method and mandates that the per capita claims costs used in the valuation be age-adjusted – not simply the blended premiums charged by the employer.

1. Determine age-adjusted per capita costs

Following ASOP 6 guidance, the actuary develops what it would actually cost to provide healthcare for each age cohort separately. These costs are typically derived from insurance carrier data, published age-adjustment factors, or plan experience.

For example, a 64-year-old retiree may have an expected healthcare cost of $1800 per month, while a 45-year-old active employee costs $450 per month, even if both individuals are charged the same $900 blended premium.

2. Project those costs forward

The age-adjusted costs are then projected forward using healthcare trend rates, which reflect expected medical inflation over time. GASB 75 requires explicit healthcare trend assumptions, and those assumptions may differ by category of expense such as hospital services, physician services, or prescription drugs.

3. Calculate the Total OPEB Liability (TOL)

Using the entry age method, the actuary attributes the projected value of each employee’s future benefits across their working career as either a level percentage of pay or level dollar amount.

This produces the Total OPEB Liability (TOL), which represents the present value of all benefits earned to date. The liability is discounted at either:

- the expected long-term investment return for funded plans, or

- a municipal bond index rate for unfunded plans.

4. Where the Implicit Cost Appears:

The implicit cost becomes visible when age-adjusted costs are used instead of the blended premium structure. Because retiree healthcare costs are significantly higher than the blended premiums often charged to retirees, the projected future benefit payments become materially larger than a simple “project the premium” approach would suggest. That increase in projected future costs directly increases the TOL.

In other words, the increase in the TOL resulting from age-adjusted costs is the recognition of the implicit subsidy embedded within the premium structure.

5. Required Financial Statement Disclosure

GASB 75 requires governments to report:

- The Total OPEB Liability (TOL),

- The Net OPEB Liability (TOL minus any plan assets), and

- Related deferred inflows/outflows

Directly on the face of the financial statements rather than solely in the footnotes, as was common under GASB 45.

This makes the implicit cost visible to bondholders, taxpayers, and oversight bodies in a way it previously was not.

Why Many Governments Were Surprised

Many governments believed they had relatively small OPEB obligations because retirees were paying what appeared to be their “fair share” of premiums.

However, GASB 75’s age-adjusted measurement framework reveals that the blended premium structure itself is a form of benefit with a measurable and potentially very large present value. Because of that, many governments were surprised by how much their OPEB liabilities grew when they adopted GASB 75.

What Happens If the Implicit Cost Is Ignored?

When the implicit cost is ignored, the OPEB liability is systematically understated. However, the consequences ripple further than just a number on a balance sheet.

The Direct Measurement Error

If an actuary projects the blended premium instead of age-adjusted costs, the assumed retiree healthcare cost is understated. Since the Total OPEB Liability represents the present value of projected future benefits, understating the per-retiree cost directly understates the liability itself.

For plans with large retiree populations or long post-retirement coverage periods, the understatement can be substantial — often ranging from 20% to 50% depending on the demographics of the group.

The Downstream Financial Impact

The understatement doesn’t stay isolated. It cascades through several related figures.

The Net OPEB Liability (TOL minus plan assets) is understated by the same amount, making the government’s balance sheet look stronger than it truly is.

Annual OPEB expense is also too low, because the service cost component (the portion earned by employees during the current year) is calculated using the same flawed per capita assumptions. This means operating results are overstated year after year.

For governments that prefund OPEB obligations, actuarial contribution calculations may also be insufficient, leading to chronic underfunding that compounds over time as the retiree population ages and the true costs eventually become unavoidable.

The Long-Term Fiscal Impact

The implicit subsidy generally grows as:

- More employees retire,

- Retirees live longer, and

- Healthcare costs continue rising faster than general inflation.

Ignoring the subsidy therefore creates more than a one-time error. The gap between the reported liability and the true liability widens each valuation cycle.

When the issue is eventually corrected – whether through an actuarial assumption update, auditor review, or change in methodology – the liability can spike dramatically in a single year, creating a fiscal shock that is much harder to manage than gradual recognition would have been.

Audit and Compliance Risk

GASB 75 is explicit that age-adjusted costs must be used in measuring OPEB obligations.

Auditors reviewing OPEB disclosures are expected to evaluate whether the actuary’s per capita claims cost development complies with ASOP 6 guidance. If blended rates are used without appropriate justification, the financial statements may be materially misstated.

This can expose governments to:

- Audit findings,

- Restatements, and

- Reputational concerns with bond rating agencies.

The Rating Agency Dimension

Credit rating agencies such as Moody’s, S&P global ratings, and Fitch Ratings all incorporate OPEB liabilities into their analysis of government creditworthiness.

An understated OPEB liability can mask fiscal stress that rating analysts may identify independently through their own adjustments and modeling.

Governments that understate their OPEB obligations do not necessarily fool the market – they just make their disclosures less credible.

Why Implicit Cost Matters

Ignoring implicit cost is not a conservative accounting choice, it’s an error that defers recognition of a real obligation.

The cost of providing healthcare to an aging retiree population does not disappear simply because the premium structure obscures it. GASB 75 exists precisely to prevent governments from treating a hidden subsidy as if it were not subsidy at all.

Additional Resources

For readers looking for a deeper technical discussion of implicit rate subsidies in OPEB plans, the Society of Actuaries has published additional guidance and analysis here:

Accounting for the Implicit Rate Subsidy in OPEB Plans (SOA PDF)

Related Reading

- Understanding Implicit Subsidies in OPEB Plans

- Difference between GASB 74 and GASB 75

- OPEB valuation services

Understanding how implicit cost impacts your OPEB valuation is critical for accurate financial reporting under GASB 75. If your organization is evaluating retiree healthcare obligations, reviewing actuarial assumptions, or preparing for an upcoming valuation, Odyssey Advisors can help you better understand how these liabilities are being measured and disclosed.

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author

Explore More Resources