Can I Contribute to a SIMPLE IRA and 401(k) in the Same Year?

Bottom Line Up Front

- You can contribute to both a SIMPLE IRA and a 401(k) in the same year, but your employee salary-deferral limit is shared across both plans — for 2026, that combined cap is $24,500, not two separate maximums.

- Business owners cannot simply run both plans side by side — to switch from a SIMPLE IRA to a 401(k), the SIMPLE IRA must be terminated, either at year-end or mid-year under SECURE 2.0’s safe harbor 401(k) replacement rules.

- A mid-year switch comes with a prorated deferral limit, meaning if you’ve already contributed heavily to the SIMPLE IRA, your remaining 401(k) employee deferral room for that year will be reduced — though employer contributions can help close the gap toward the $72,000 annual additions limit.

Yes, you can contribute to a SIMPLE IRA and a 401(k) in the same year if you are eligible for both plans, such as when you change jobs, work for two unrelated employers, or have a job plus self-employment income. But there’s a catch: your employee salary-deferral limit is shared across both plans. You do not get to contribute to the full SIMPLE IRA employee limit and the full 401(k) employee limit separately.

For 2026, the general employee deferral limit for a traditional or safe harbor 401(k) is $24,500, and the general SIMPLE IRA salary-reduction limit is $17,000. The IRS states that if you participate in a SIMPLE IRA and another employer plan in the same year, the total salary-reduction contributions you make across all such plans are limited to $24,500 for 2026, before any applicable catch-up contributions.

Can a Business Owner Switch from a SIMPLE IRA to a 401(k) and Contribute in the Same Year?

For many small business owners, a SIMPLE IRA is a good starter retirement plan. It is relatively easy to set up, inexpensive to operate, and generally does not require the employer to file an annual Form 5500. But once your business is profitable enough that you want to contribute much more for yourself, the SIMPLE IRA can start to feel limiting. The 401(k), especially when paired with employer profit-sharing contributions, can offer a much higher ceiling.

For 2026, the annual 401(k) employee elective deferral limit is $24,500, while the total annual additions limit for a 401(k) or profit-sharing plan is $72,000, not counting catch-up contributions. By comparison, the general SIMPLE IRA employee salary-reduction limit is $17,000 for 2026, with required employer contribution typically limited to a 3% match or a 2% nonelective contribution formula.

So, can you contribute to a SIMPLE IRA and a 401(k) in the same year if you own the business and want to switch plans? The answer is: sometimes, but not by simply running both plans side by side.

The key point to make the switch from a SIMPLE IRA to a 401(k) is that the 401(k) must replace the SIMPLE IRA, you cannot simply add a 401(k) on top of an existing SIMPLE IRA.

How Do You Switch from a SIMPLE IRA to a 401(k)?

There are two practical ways to move from a SIMPLE IRA to a 401(k):

The first is the clean year-end switch. You discontinue the SIMPLE IRA effective January 1 and start the 401(k) for the new plan year. The IRS says that, for a standard SIMPLE IRA termination, you notify employees before November 2 that the SIMPLE IRA will be discontinued effective the following January 1, notify the financial institution and payroll provider, and keep records of your actions.

But let’s say you add a few big customers, and you want to start getting the bigger tax deduction this year. The second option is a mid-year replacement. Under SECURE 2.0 for plan years beginning after 2023, an employer can terminate a SIMPLE IRA during the year if it establishes and maintains a safe harbor 401(k) to replace it – it will require a 30 day notice vs the traditional 60 day notice for a January 1st plan change. In that case, the safe harbor 401(k) is treated as an exception to the normal rule that prevents an employer from maintaining both a SIMPLE IRA and another plan in the same calendar year.

For a business owner whose main goal is to contribute the full $72,000 between employee and employer contributions, the cleanest planning route is usually to terminate the SIMPLE IRA at year-end and start the 401(k) on January 1. For some it may be worth the extra effort to make the switch immediately and take advantage of the added contributions and tax deductions a 401(k) offers.

Want to Upgrade Your SIMPLE IRA to a 401(k) Plan in 2026?

What Happens if You Switch from a SIMPLE IRA to a 401(k) Mid-Year?

A mid-year switch is possible, but it is not as simple as saying, “I contributed to the SIMPLE IRA for part of the year, now I’ll contribute the full 401(k) maximum.”

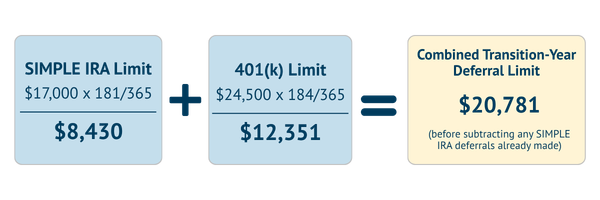

When a SIMPLE IRA is replaced mid-year by a safe harbor 401(k), the IRS requires the employee deferral limit for the transition year to be calculated using a weighted formula. The formula prorates the SIMPLE IRA limit for the part of the year the SIMPLE IRA was in effect, prorates the 401(k) limit for the part of the year the safe harbor 401(k) was in effect, and then subtracts any SIMPLE IRA salary-reduction contributions already made that year.

For example, assume the SIMPLE IRA is in place from January 1 through June 30, 2026, and the safe harbor 401(k) starts July 1. Ignoring catch-up contributions, the weighted employee deferral limit would be approximately:

This creates a combined transition-year deferral limit of about $20,781, minus whatever you already deferred into the SIMPLE IRA.

If you had already deferred the full $17,000 into the SIMPLE IRA before the switch, your remaining employee deferral room for the 401(k) would be only about $3,781 in this example.

That does not necessarily mean the $72,000 goal is impossible, but it does mean the employee-deferral portion may be smaller, and more of the contribution would need to come from the employer side if allowed. In addition, a mid-year 401(k) can create short-plan-year or short-limitation-year issues, and the IRS notes that the Section 415 annual additions limit may need to be prorated in a short limitation year depending on how the plan is drafted.

Key Takeaways: Moving a SIMPLE IRA to a 401(k)

Switching from a SIMPLE IRA to a 401(k) can be an effective way for business owners to increase retirement contributions and potentially generate larger tax deductions. However, the transition must be handled carefully. In most cases, you cannot simply add a 401(k) on top of an existing SIMPLE IRA without first terminating or replacing the SIMPLE IRA according to IRS rules.

While a 401(k) generally involves more administration and recordkeeping than a SIMPLE IRA, the increased contribution flexibility may make the additional complexity worthwhile. If you’re considering making the switch, it’s important to coordinate with your retirement plan advisor, TPA, payroll provider, and tax professional to ensure the transition is completed correctly and to maximize available contribution opportunities.

Frequently Asked Questions

Can I max out both a SIMPLE IRA and a 401(k) in the same year?

No. The employee salary-deferral limit is generally shared across both plans, so you cannot contribute the full employee maximum to each separately.

Can I have a SIMPLE IRA and a 401(k) at the same time?

Generally, an employer cannot maintain both plans simultaneously unless a specific exception applies, such as the SECURE 2.0 mid-year replacement rules.

Is it worth switching from a SIMPLE IRA to a 401(k)?

For many growing businesses, a 401(k) provides significantly higher contribution opportunities and greater plan design flexibility, though it comes with additional administrative responsibilities.

About The Author Kurtis has been a consultant on the Odyssey Advisors team since 2013 and has developed extensive knowledge and expertise in developing and administering retirement benefit solutions. Kurtis is passionate about helping people achieve the retirement they’ve always dreamed of...

More Insights From This author

Explore More Resources