Mega Backdoor Roth & After-Tax Contributions in Your 401(k) Plan

Bottom Line Up Front

- Making contributions to your company’s 401(k) plan and then transferring the balance to a Roth 401(k) can allow you to increase contributions and help decrease your taxes.

- In 2026, a participant can contribute up to $24,500 from their pre-tax earnings and up to $47,500 after taxes into their 401(k) plan for a total of up to $72,000 (indexed) — not including catch-up contributions.

- The Mega Roth Backdoor IRA can be effective under a plan with ideal demographics and generous employer contributions to save more in a Roth IRA or Roth 401(k) than you would normally be able to.

You know that Mega Backdoor Roth thing your friend mentioned or that you stumbled across online? The one where you can make substantial contributions to your employer-sponsored 401(k) plan and then transfer them to a Roth 401(k) essentially saving you more on taxes in the long run. It may sound too good to be true, but it can work wonders for those who qualify and are in the right plan. It’s especially helpful if you’d typically be unable to contribute to a Roth account due to exceeding income limits.

The Logistics

Under the IRS Code, 401(k) plans have a variety of contribution limits (excluding catch-up contributions):

- Employee Deferral – $24,500 for 2026 (indexed)

- Maximum Account Addition – $72,000 for 2026 (indexed)

Beyond that, 401(k) plans have various non-discrimination rules to ensure that the plan does not overly benefit highly compensated employees (“HCEs”). As it relates to this situation, the key testing is the ADP/ACP test.

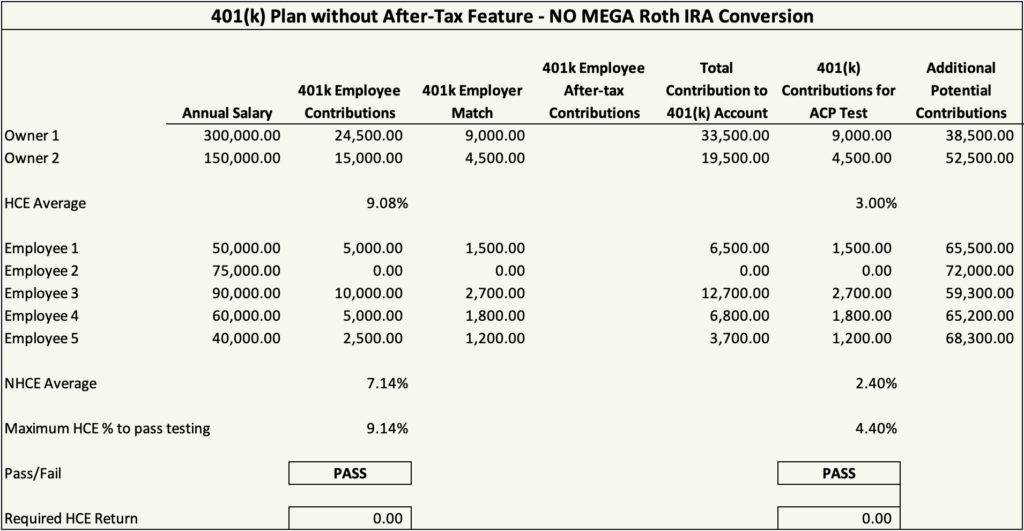

As an example – we have a small company with two (2) owners and five (5) employees. The plan has reasonable participation with the employees on average contributing 7.14% of their pay and an employer match of 50% up to 6.0% of pay deferred yielding a Non-Highly Compensated Employee (“NHCE”) Average Contribution Percentage (“ACP”) of 2.40% for our NHCE group.

Based on these figures our owner’s contributions of 9.08% as employees and the employer match ACP of 3.00% allows them to easily pass our ADP & ACP tests.

Now, let’s add an after-tax feature to our plan. The owners see that they are far from their $72,000 total contribution limit and they have additional money they’d like to save for retirement. Owner 1 contributes the full $38,500 of that potential $38,500 available to maximize their account to the after-tax source in the plan. It’s important to remember that after-tax contributions are treated as employer contributions for purposes of the ACP test.

So, let’s see what happens:

The ADP test still passes easily as there was no change. However, they now fail the ACP test and the Owner 1 will be required to take a return of $22,575 in excess after-tax contributions – that’s not going to be a pleasant conversation for the TPA to have with them.

So, what’s the big deal? I put money in, and I get it back if we fail?

Well, let’s remember the objective here. You were putting money into the after-tax source with the goal of immediately converting it to a Roth either within the plan or via an in-service distribution to a Roth IRA. Well, that conversion/rollover would be ineligible and would need to be disgorged from their account – and you thought the 1st TPA conversation with Owner 1 was going to be rough!

Bottom Line

The Mega Backdoor Roth can and does work. But you need to have ideal demographics and likely a very generous employer contribution to the plan. If so, this can be a great benefit.

The short answer – talk to your TPA or consultant, evaluate the demographics and objectives, and do a preliminary ACP test in advance to see if it will work.

If you’d like to know more, you can reach out to us here. We’d be happy to help answer any questions you may have.

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author