What is a Cash Balance Plan? Your Top Questions Answered

Bottom Line Up Front

- A Cash Balance Plan is a type of Defined Benefit Plan that allows large tax-deductible retirement contributions that are tax-deferred and protected from creditors.

- These plans are ideal for business owners and self-employed individuals who want to ramp up their retirement savings while reducing their tax burden.

- Typically, Cash Balance plans work best for people 50 and older, with stable, predictable, high income.

What is a Cash Balance Plan?

A Cash Balance Plan is a Defined Benefit Pension Plan, IRS § 401(a), often used by small business owners. It allows for significant tax-deductible contributions and retirement asset accumulation. Contributions are tax-deferred, and your assets are protected from creditors. In short, it’s an excellent tool for tax planning, asset accumulation, and asset protection.

Key Benefits of a Cash Balance Plan

Most business owners adopt a Cash Balance Plan to supercharge their retirement savings while taking advantage of generous tax deductions. Unlike 401(k) Profit Sharing Plans, these plans offer higher annual contribution limits, which means you can put away more for retirement and defer more taxes.

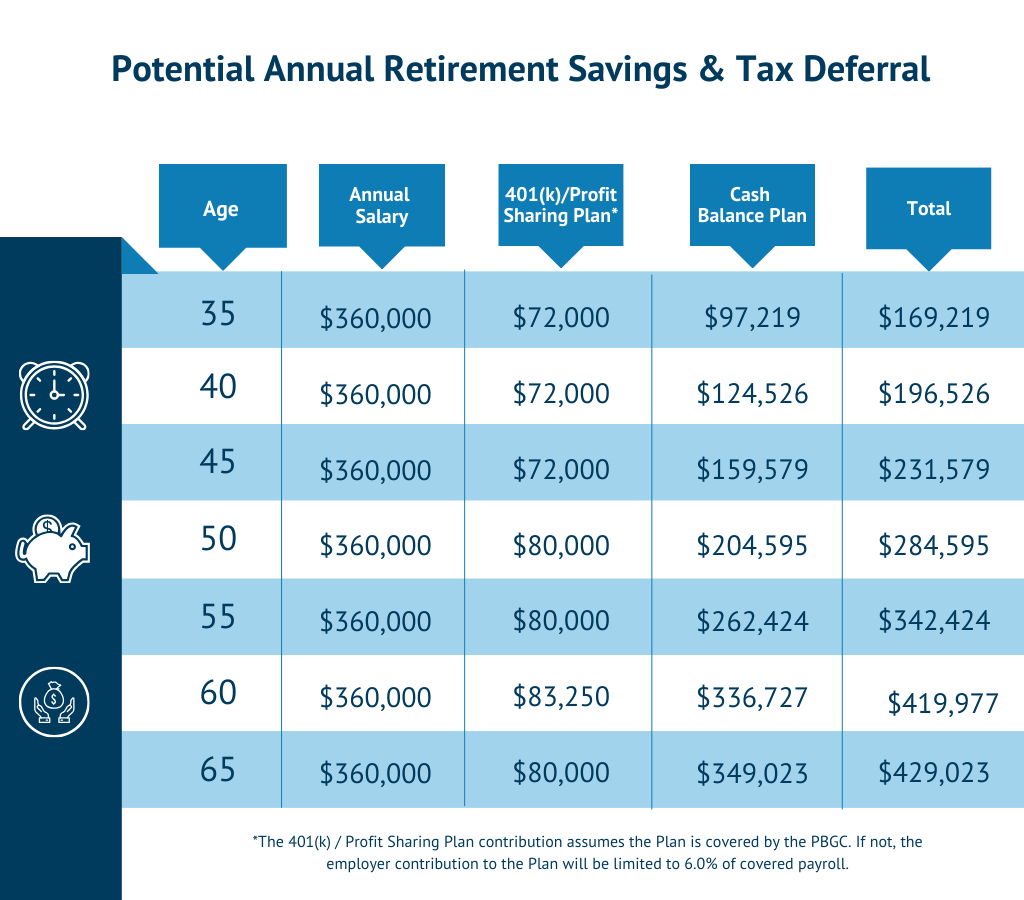

Potential Annual Retirement Savings & Tax Deferral for 2025

For a full breakdown of the 2026 cash balance plan and 401(k) contribution limits by age, see our 2026 CB Plan Contribution Limits PDF.

What is the difference between a Cash Balance Plan and a 401(k) Plan?

Both Cash Balance and 401(k) Plans are considered “qualified plans” under IRS § 401, but there’s a key difference:

- Cash Balance Plan: Defined Benefit Plan – the retirement benefit is defined, not the contribution.

- 401(k) Plan: Defined Contribution Plan – the contribution is defined, not the retirement benefit.

In a 401(k) plan, the employee assumes the investment risk. With a Cash Balance Plan, the employer bears that responsibility. Plus, Cash Balance Plans must offer a lifetime annuity option and are typically backed by the Pension Benefit Guaranty Corporation (PBGC), which provides insurance for such benefits.

Can I have a Cash Balance Plan if I already have a 401(k) or IRA?

Yes! Cash Balance Plans aren’t designed to replace your 401(k) or IRA – they’re meant to complement them. Think of it as stacking multiple retirement plans to maximize your savings potential.

Who Should Consider a Cash Balance Plan?

A Cash Balance Plan may be a good fit for you and your business if:

- Your company has fewer than 10 employees.

- The owners are typically older than the employees.

- You have a stable, high income with some predictability.

How does a Cash Balance Plan work?

Each participant in a Cash Balance Plan gets a “pay credit” every year, which is the amount the employer contributes on their behalf. The contribution can be a flat dollar amount or a percentage of income and may vary between employees and owners, as long as it passes compliance testing. For example, $1,000 annually per participant or 3% of a participant’s annual income. Each company’s funding formula varies based on the employer’s goals and their employee demographics.

Additionally, accounts earn interest on accumulated contributions each year, called interest credit. Usually, a fixed rate like 5% or tied to an index, such as the 30-year Treasury yield.

Self-employed? Yes, You Can Set Up a Cash Balance Plan

If you’re self-employed, a Cash Balance Plan can be a powerful retirement tool. You can combine it with other plans to significantly increase your retirement contributions.

What is the maximum amount I can get from a Cash Balance Plan?

As noted above, a Cash Balance Plan is a defined benefit plan, so there are limits on the maximum benefit that may be paid. IRS § 415(b) limits the benefit that may be paid from a defined benefit plan ($285,000 annually at Normal Retirement Date for 2026, indexed). This amount is reduced if the participant has less than 10 years of participation in the plan, as well as for retirement before the Normal Retirement Date. Assuming that the participant is at least age 62 with a minimum of 10 years of participation in the plan, the maximum lifetime lump sum payable from a Cash Balance plan is approximately $3.6 million for 2026 (indexed based on interest rates, mortality, etc.).

How much can I contribute to a Cash Balance Plan?

The maximum amount you can contribute is limited by your compensation and age. For example, if you earn $360,000, you could roughly contribute:

- $195,000 at age 40

- $280,000 at age 50

- $415,000 at age 60

Does a Cash Balance Plan Affect My 401(k) Contributions?

The tax deduction limit for the combined plans (Cash Balance & 401k) is greater than 25% of covered payroll and the minimum required funding for the Cash Balance Plan. However, if employer contributions to the 401(k) Plan do not exceed 6.0% of covered payroll, the 25% limit does not apply. If the Cash Balance Plan is covered by the PBGC, higher contribution limits will apply.

How is My Cash Balance Benefit Determined?

There are three main components to your Cash Balance benefit:

- Pay Credits – Contributions are typically a percentage of compensation (typically on an annual basis).

- Interest Credits – Usually a fixed rate or tied to an index (like the S&P 500 or Treasury rates). The interest credit frequency is defined by the plan but is normally credited annually.

- Actuarial Equivalence – The plan outlines how the balance is converted to a benefit (lump sum or annuity) at retirement.

Can I Use a Vesting Schedule?

Absolutely! Cash Balance Plans can use a vesting schedule, typically no more than three years. Many plans use “cliff” vesting, where you’re 100% vested after three years, though some use graded schedules with partial vesting sooner. When an employee terminates employment before completing the required vesting service for 100% vesting, any non-vested amount is “forfeited” and may be used to offset or reduce the employer’s future contributions.

How Long Do I Need to Keep the Plan?

All qualified retirement plans, including Cash Balance plans, must be intended to be “permanent” at inception. While there’s no hard rule, it’s generally recommended to keep a plan in place for at least five years to meet the permanency requirement. However, unforeseen circumstances like a business sale or revenue change could justify an early termination.

Advantages & Disadvantages

The advantages are well known and often highlighted, but it is important to remember that large tax-deductible contributions and flexible plan design do carry the disadvantage of minimum required contributions.

| Advantages | Disadvantages |

| Large tax-deductible contributions | Employer bears investment risk |

| Flexible plan design | Mandatory annual contributions |

| Simple, easy-to-understand benefits | Requires annual actuarial certification |

| Lump-sum payouts at retirement | More expensive to administer than a 401(k) Plan |

Investing Cash Balance Plan Assets

Unlike a 401(k) Plan, a Cash Balance Plan’s assets are pooled and invested by the employer. You should work with your investment advisor to determine an appropriate investment policy given the plan’s defined interest crediting method and the plan sponsor’s tolerance for contribution volatility.

A conservative to moderate asset allocation (with 3-7% per year) is common to manage contribution volatility and prevent overfunding.

Is a Cash Balance Plan Right for You?

If you’re self-employed or own a business with steady income, are over 35, and want to boost your retirement contributions, a Cash Balance Plan could be a smart move. These plans are very common for professional services firms, but they work for any business with predictable income.

There are a lot of factors to consider when adding a new retirement plan as a business owner. An actuary who specializes in retirement plans, specifically defined benefit and cash balance plans, can help you understand if a Cash Balance plan is right for you based on your situation and goals.

What is the deadline to establish a new Cash Balance Plan?

With the passage of the SECURE Act, the deadline to establish a plan is the business’s tax filing deadline (including extensions). The plan must be both executed and funded by that deadline, so it is important to begin working with an actuary and your financial professional well in advance of that date to ensure you can meet the deadline.

How Do I Set Up a Plan?

Start by working with an actuary to design the plan that fits your goals. You’ll also want to work with your financial advisor to establish a trust for plan investments. It’s best to allow four to six weeks for everything to be in place.

If you have questions on how to align your business needs with your personal goals, check out our form below. If you would like to get a free retirement plan review, you can reach out to us directly here.

Categories: Defined Benefit Plan, Retirement

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author

Explore More Resources