Pension Lump Sum Values to Plunge in 2023

Bottom Line Up Front

- Many Defined Benefit pension plans offer retirees two options: a fixed monthly payment for life or one large lump sum payment.

- Each year, lump sum values are recalculated using the minimum present value segments rates provide by the IRS which means the payment may vary year to year.

- Lump sum values for 2023 will take a plunge, but there’s still time to claim your benefit in 2022 before the recalculation takes place.

If you or one of your clients is covered by a Defined Benefit pension plan that offers lump sum payments and they are eligible to retire, they may wish to consider doing so in 2022 vs waiting until 2023.

When it comes time for retirement, retirees with pensions often have two options: fixed monthly payments or one lump sum payment. A difficult aspect of this decision is that lump sum payments may vary from year to year. This makes deciding when to retire even more challenging.

Each plan has lump sum equivalency factors, but they are subject to IRC Section 417(e)(3)(D) which defines the minimum that must be paid (many plan documents set the equivalency factors equal to the IRS minimum). So given the recent increases in interest rates, we will see lump sum values plunge in 2023.

The good news is that pension plans won’t be recalculating your benefits until 2023 so there’s still time to claim your lump sum offer for 2022.

I thought benefits were protected and could never be reduced?

It’s important to remember that the plan’s Accrued Benefit is defined as a monthly benefit payable at the plan’s Normal Retirement Date. So, it’s correct that IRC Section 411(d)(6) does NOT allow for an Accrued Benefit to be reduced but the lump sum payment is a “form of payment” and not the accrued benefit.

What are the interest rates that the IRS sets for a minimum lump sum benefit?

The IRS publishes “segment rates” each month for benefits payable in the 1st five years of distribution, the next 15 years and all payments thereafter (https://www.irs.gov/retirement-plans/minimum-present-value-segment-rates). Each plan defines their “Stability Period” and “Applicable Month” differently – you can find it in the plan document or Summary Plan Description.

What is the magnitude of the change?

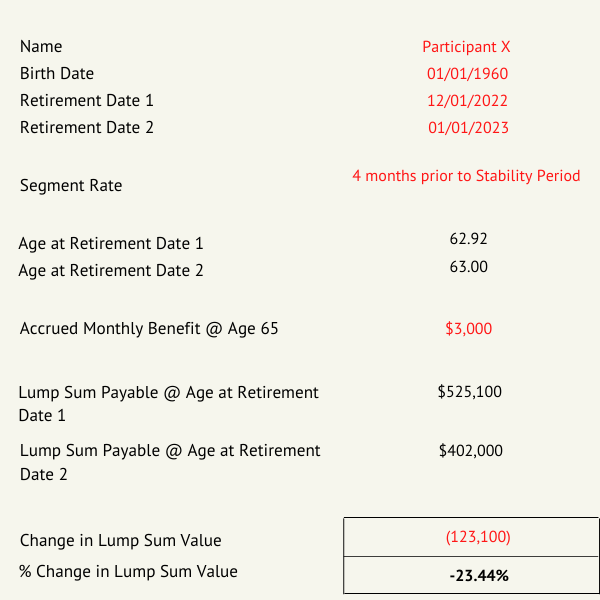

For example, a participant with a $3,000 per month frozen Accrued Benefit payable at age 65 who is eligible to retire at age 62, the impact of a December 2022 vs January 2023 benefit commencement date is a reduction of over 23% of the lump sum payable, or approximately $123,000. Take a look at the example below:

What should I do about it?

Ultimately, the choice of when to retire or terminate employment is a personal one and the lump sum value of your retirement benefit is only one component of that decision. However, if your retirement planning is based on a lump sum payment, you should review your retirement options with your financial team and evaluate your options.

If you have additional questions or need more information, please contact me or any of our Odyssey consultants.

Categories:

Share