What Are the Advantages and Disadvantages of an OPEB Trust?

KEY POINTS

- A majority of state government entities have large unfunded OPEB liabilities.

- Establishing an OPEB Trust can help mitigate your liabilities, increase your credit rating, and enhance generational equity.

- You must also keep in mind the costs associated, the time and resources needed to govern the trust, and that the funds can only be used for other post-employment benefits.

I’m going to cut to the chase and give you some facts: in 2016 the total other post-employment benefits (“OPEB”) liability stood at $696 billion while states only had $46 billion in assets to take care of these benefits according to a study by Pew. That’s about 6% of the nation’s total OPEB liability (“TOL”).

What’s OPEB?

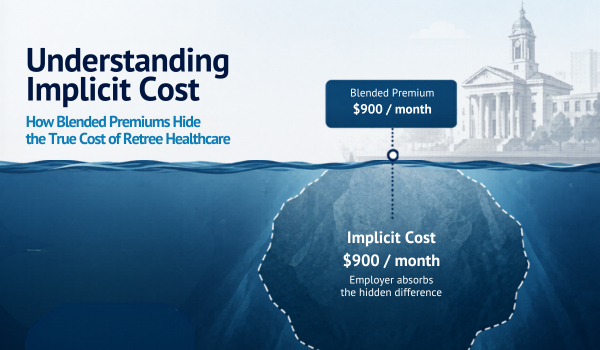

OPEB stands for other post-employment benefits which are benefits that state and local governments give to their employees at retirement, other than their pension. The most common of these benefits are medical, dental, and life insurance.

OPEB Funding

If you’re reading this and you’re a government employer, whether that’s a Town, City, School District, Utility District, etc., and offer OPEB to current and former employees, you should start thinking about establishing an OPEB Trust. Many municipalities are currently considering pre-funding their OPEB liabilities and wondering if it makes sense. Here are some things you should know:

What are the Advantages of Having an OPEB Trust?

As an OPEB plan sponsor, I can almost guarantee that your actuary, auditor, bond consultant, or a combination of all three, have mentioned establishing an OPEB Trust, but you’re not sure if it would be beneficial for you. Here’s everything you need to know:

- It shows financial management and stability. The creation, funding, and management of an OPEB Trust signals to the credit rating agencies as well as the broader public that your organization is looking to manage these large unfunded liabilities (which are often one of the most significant unfunded liabilities on a government entity’s balance sheet along with pension obligations). Funding this obligation as it occurs will provide future financial statement flexibility and enhances your ability to pay your debt service.

- Investment returns may help pay for benefits. While general governmental funds are usually subject to strict limits on any investment choices (often bank accounts or U.S. Treasuries) which offer modest yields even in the best of times, the OPEB Trust will normally allow for a wider net of investments across the various asset classes (e.g., stocks, bonds, real estate, etc.). While investment returns are not guaranteed, the OPEB Trust is generally invested for the long-term and is projected to have higher returns than general governmental funds – these excess returns may be used to reduce the long-term cost of the OPEB plan.

- It enhances generational equity. The current pay-as-you-go funding model results in the need for your future taxpayers to provide the resources to pay for those OPEB benefits when they come due many years in the future. The rationale for an OPEB Trust is that the plan sponsor and taxpayer of today will fund benefits that are earned today so that these costs are not borne by a future taxpayer.

- It secures these assets from creditors. Municipal bankruptcy is rare, but lawsuits against these entities are not. If your assets are held in a properly constructed OPEB Trust, they are legally protected from creditors.

What are the Disadvantages of an OPEB Trust?

- The funds may only be used for OPEB. You do not have the same level of access to the funds in the OPEB Trust as you do with general governmental funds. These funds may only be utilized to pay for OPEB benefits until there are no further benefits to be paid. As such, they may not be used to meet other needs of your municipal organization or offset other tax and spending priorities.

- They require governance. As the sponsor of the OPEB Trust, your municipal organization must make decisions on how assets will be held, how they will be invested, how they will be disbursed, and provide oversight of the service providers.

- The costs associated with a Trust. Like any product or service, there is a cost – either implicit or explicit. If your municipal organization is funding a material amount each year, you will accumulate sufficient assets quickly which will mitigate the costs. However, if the OPEB Trust has a very low level of assets and/or your organization chooses to limit their contributions, the costs of the Trust may not make economic sense.

So, What Should You Do?

Each municipal organization must make its own decision, but the GFOA considers it a best practice to create and fund an OPEB Trust. At a minimum, we suggest you work with your actuary to review potential funding scenarios to see what may be possible given your organization’s current and future cash flows. In doing so, you will be securing these benefits for current and future retirees while also stabilizing the future financial stability of your organization.

Interest in Learning More?

Pension Contributions at Risk due to COVID-19

2020 Year-End OPEB Trend Report

Municipal Borrowing at 10-Year High and What It Means For You

Categories: OPEB

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author