When Can You Withdraw from an OPEB Trust?

Bottom Line Up Front

- An OPEB Trust must meet three criteria: it must be irrevocable, protected from creditors, and only used to pay for OPEB benefits

- If the annual funding exceeds the annual Service Cost, a plan sponsor may feel it’s appropriate to begin withdrawals from the plan

- Make sure to review your plan’s funded ratio and if it falls below 50%, it may be wise to hold off on making any withdrawals.

So, you sponsor an Other Postemployment Benefits (“OPEB”) Plan, and your municipality entity established an OPEB Trust and is actually funding it. Now your stakeholders are asking, “Is this just something where we make contributions, or is it like a pension plan where it can actually pay benefits?”

Let’s start with some basics first:

What is an OPEB Trust?

To be classified as an OPEB Trust, your fund or account must meet three (3) criteria:

- It must be irrevocable – this means that this fund may not be revoked or canceled until all such funds have been utilized to pay OPEB benefits or the OPEB Plan is terminated and no further benefits are due.

- It must be protected from creditors – this means that it is not an asset of the plan sponsor but a stand-alone fund. As such, if the plan sponsor is sued or has a judgment against it, these funds are insulated and may not be attached to pay any such judgment.

- It may only be used to pay OPEB benefits – these funds may not be redirected to meet other needs beyond other post-employment benefits.

What is a Service or Normal Cost?

A Service Cost is the value of benefits to be earned during the year by active employees.

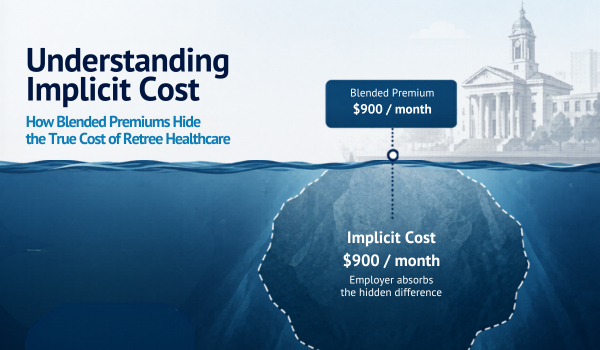

What is the Pay-As-You-Go Expense?

The pay-as-you-go expense represents the employer’s share of costs for all OPEB benefit payments such as healthcare, dental, or life insurance premiums (and any “implicit” cost or subsidy) for retirees in pay status.

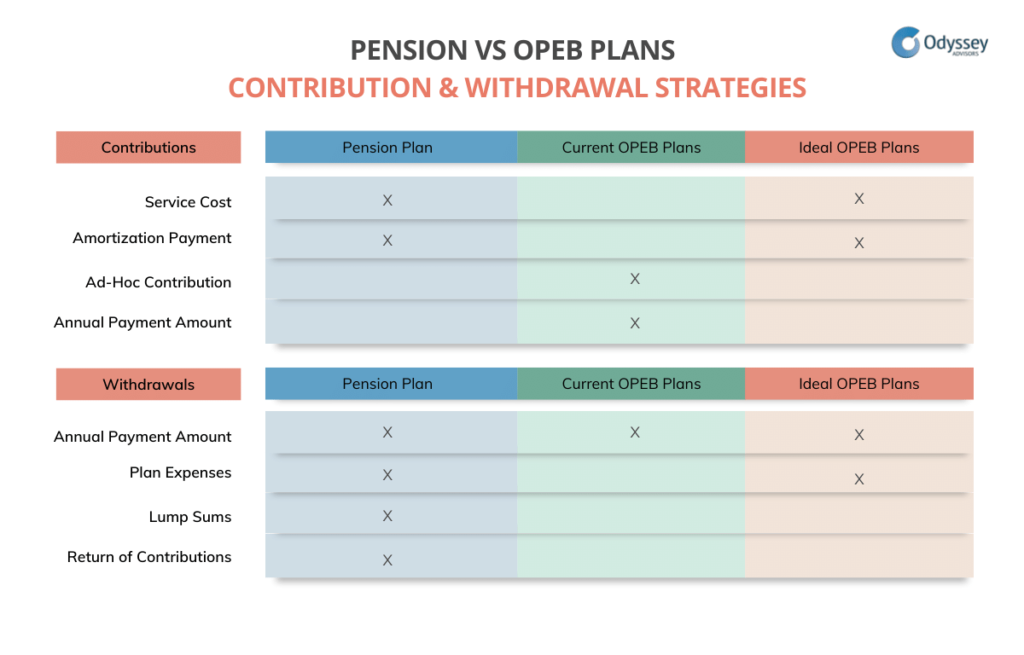

Pension and OPEB Plan Contribution & Withdrawal Strategies

The funding of an OPEB plan or Trust is very similar to your pension system except that very few OPEB plans have a statutory funding requirement or appropriation schedule.

Let’s review how a pension system is normally funded for comparison purposes:

Pension contributions are normally comprised of two components:

- The annual Service Cost

- Amortization of the unfunded liability. (If the plan is fully funded, the contribution will just be the annual Service Cost.)

Pension withdrawals comprise monthly benefit payments, lump sum payments, plan expenses, and any returns of contributions.

In the OPEB context, we see the following:

OPEB contributions normally comprise of the annual pay-as-you-go costs plus some additional amount to reduce the unfunded liability (this amount may be an amortization schedule but is often based on the sponsor’s ability to pay). Generally, sponsors will not actually contribute to the pay-as-you-go costs. Instead, they will pay the costs from general revenue, which is equivalent.

OPEB trust withdrawals normally consist of the annual pay-as-you-go contributions (these may be paid directly from general revenue but that effectively acts as a contribution to and withdrawal from the OPEB trust.

The difference between OPEB & Pension contributions is that the pension figure is based on service costs while the OPEB figure is based on pay-as-you-go costs. So, if the OPEB plan sponsor contributes the service cost plus some amount toward the unfunded and then chooses to have the plan pay the annual pay-as-you-go costs, that will work similarly to a pension plan.

The reality is that most OPEB Plans have very low funded ratios so we’d still discourage this approach until the plan is at least 50% funded but it can be done.

In Summary

An OPEB plan and the Trust can be run in a similar manner to a pension plan. It ultimately is a matter of the plan’s funded status and the annual ongoing funding of the plan. If the plan has regular ongoing funding similar to a pension plan (service cost plus an amortization payment), then withdrawals are viable. However, the large majority of OPEB plans have low-to-modestly funded ratios and lack a strong ongoing funding commitment.

If you still have questions about OPEB trust withdrawal or funding strategies, you can reach me or one of our Odyssey Consultants here.

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author

Explore More Resources