What to Expect for Medicare and Social Security in 2026

Bottom Line Up Front

- Medicare costs are climbing – Part B premiums are projected to rise over 11%, and Medigap plans could see an 8-12% increase.

- Social Security COLA will be modest – Expect a 2.6% to 2.8% adjustment, adding around $50/month on average, which will be largely offset by increased Medicare premiums.

- High-income retirees may pay more – IRMAA surcharges are expected to rise slightly, so income planning now could help avoid higher costs later.

It’s almost August, which means fall, the holidays, and the new year are just around the corner. Time really does fly. As 2025 winds down, many retirees and soon-to-be retirees are already looking ahead to 2026, especially when it comes to Medicare costs and Social Security benefits.

While official numbers won’t be finalized until later this year, current projections and historical trends give us a pretty good idea of what’s coming.

Here’s a breakdown of what to expect in 2026, and a few planning tips to keep in mind.

Medicare Part B Premiums – 2026 Outlook

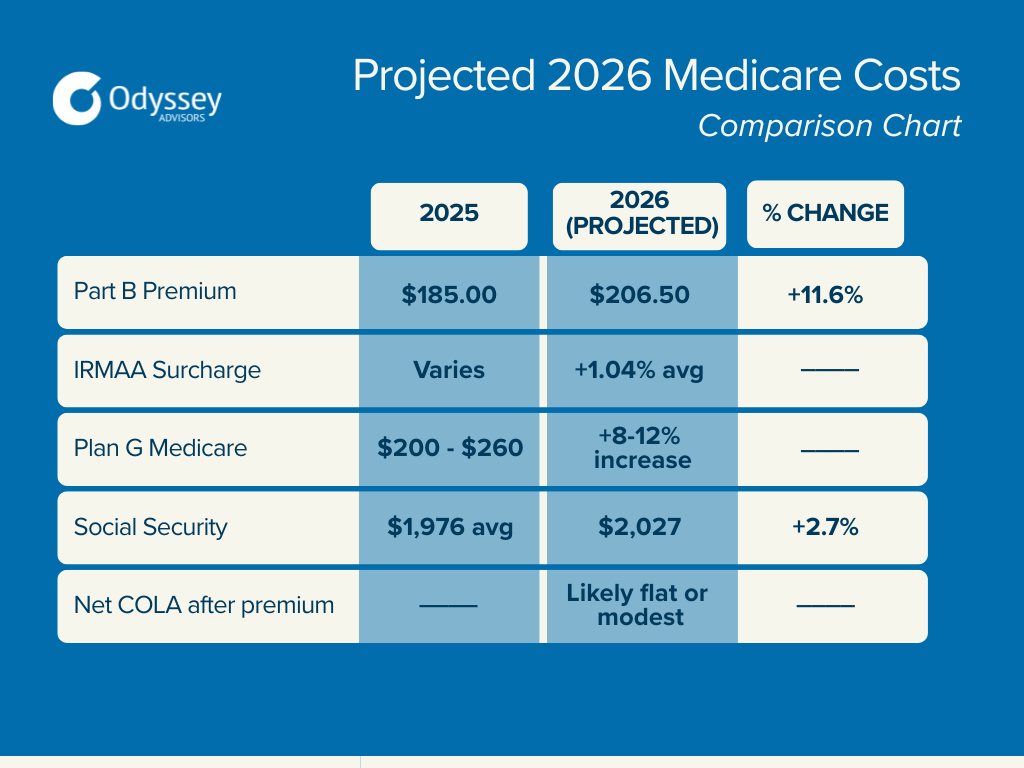

The standard Medicare Part B premium is projected to increase from $185.00 in 2025 to approximately $206.00 – a jump of $21.50 or about 11.6%.

For beneficiaries with higher incomes, IRMAA (Income-Related Monthly Adjustment Amount) surcharges are also expected to rise slightly, by an estimated 1.04% on average, according to the latest Medicare Trustees’ Report.

What this means:

- Standard Part B enrollees could pay significantly more in 2026.

- Higher-income individuals may face even greater increases due to rising IRMAA backets.

Medigap (Medicare Supplement) Premium Trends

While 2026 Medigap premiums haven’t been set yet, they typically increase annually in response to changes in Part B premiums, medical inflation, and other cost drivers.

With a projected 11-12% increase in Part B, expect Medigap plans (like Plan G or Plan N) to rise by 8-12% on average. Factors like age, gender, state, and insurer all influence final rates.

Pro tip: If you’ve had the same Medigap policy for several years, it’s worth comparing current rates with other providers or considering a different plan letter. For a look at your local Medigap plan rates, visit Medicare.gov.

Social Security Benefits & COLA – 2026 Projections

In 2025, Social Security recipients received a 2.5% cost-of-living adjustment (COLA), increasing the average monthly benefit to $1,976 for retired workers.

For 2026, most projections place the COLA between 2.6% and 2.8%, depending on inflation trends:

- 2.6% COLA: Benefit increases to ~ $2,027/month

- 2.8% COLA (optimistic): Benefit increases to ~ $2,031/month

That’s roughly a $50/month increase, on average. You can also follow updates from the Senior Citizens League as they track expected COLA changes.

But here’s the catch:

With Part B premiums also rising, many retirees may see little or no net increase in their Social Security check after deductions. In some cases, the higher premiums could completely offset the COLA increase.

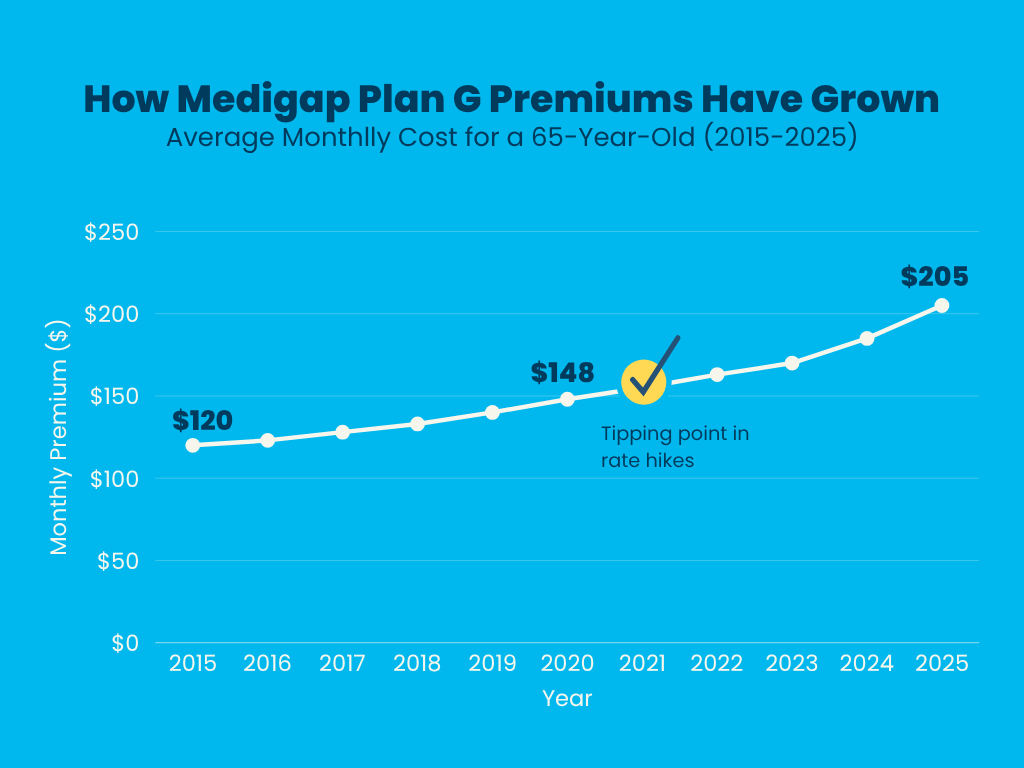

A Decade of Medigap Rate Increases (2015 – 2025)

Looking back can help us see where we’re headed. Here’s how monthly Medigap premiums for Plan G (for a 65-year-old male) have trended:

- 2015: $120 – $175

- 2020: $160 – $220

- 2025: $200 – $260

Plans F and G, the most popular options, have historically increased 5-10% per year, and the graphic (shown above) confirms a steady upward trend, particularly after 2020.

2026 at a Glance: Key Numbers

Key Takeaways for 2026

In 2026, Medicare Part B premiums are expected to rise sharply (over 11%), marking one of the most significant annual increases in recent years. Medigap plan premiums are likely to follow, with projected increases in the 8-12% range depending on plan type and location. Meanwhile, the Social Security cost-of-living adjustment (COLA) is estimated to come in around 2.6% – 2.8%, offering retirees a modest monthly benefit increase of about $50.

Unfortunately, that boost may be entirely offset by the higher Medicare premiums, leaving many beneficiaries with little to no net gain. For higher-income retirees, income-related surcharges (IRMAA) will also tick upward, making careful income planning all the more important.

What You Can Do Now

- Review your Medigap coverage. Shop around if your insurer raises rates significantly.

- Understand IRMAA thresholds. Remember, IRMAA surcharges are based on your modified adjusted gross income (MAGI) from two years prior, meaning 2024 tax returns will impact your 2026 Medicare premiums.

- Track COLA updates. The official 2026 COLA announcement comes in October 2025; stay tuned.

If you’d like approximate state-specific costs or comparisons between Medigap plans (e.g., Plan G vs. Plan N), you can reach out to us. We’re happy to help you break it all down.

Categories: OPEB, Retirement

About The Author Stephanie joined the Odyssey Advisor’s team all the way from the Lonestar state in November of 2020. She is versatile in her abilities and has experience in copywriting, photography, and analytics. She helps tell our brand story and convey...

More Insights From This author