Navigating the Changing Landscape of Medicare Part D Premiums in 2024

Bottom Line Up Front

- Medicare Part D premiums in 2024 are increasing and will significantly impact individual Medicare beneficiaries by raising their healthcare costs, and also affect local governments that sponsor OPEB plans by increasing their financial liabilities.

- The Inflation Reduction Act, although intended to reduce long-term prescription drug costs starting in 2025, contributes to the rise in Part D premiums.

- Proactive planning and informed decision-making will be key to navigating these changes successfully.

In a significant development for the 51 million Americans relying on Medicare prescription drug coverage, the Centers for Medicare & Medicaid Services (CMS) announced in July of 2023, a projected average monthly basic premium of approximately $55.50 for Medicare Part D for 2024. They claimed a 1.8% decrease from 2023, marking a rare instance of declining healthcare costs in recent times.

However, that isn’t the case for the upcoming year. Rather than seeing a decrease, there will be a significant increase in Medicare Part D premiums.

Medicare Part D: An Overview

Medicare Part D is the part of Medicare that covers prescription drugs. Offered through private insurance companies, it is a critical component of healthcare for seniors. The premiums and the drugs covered vary by plan, making it essential to stay informed about the changes and how they might impact you or your employees as they get ready to retire.

Medicare 101: Understanding the Basics

2024 Premium Increases and Its Impact

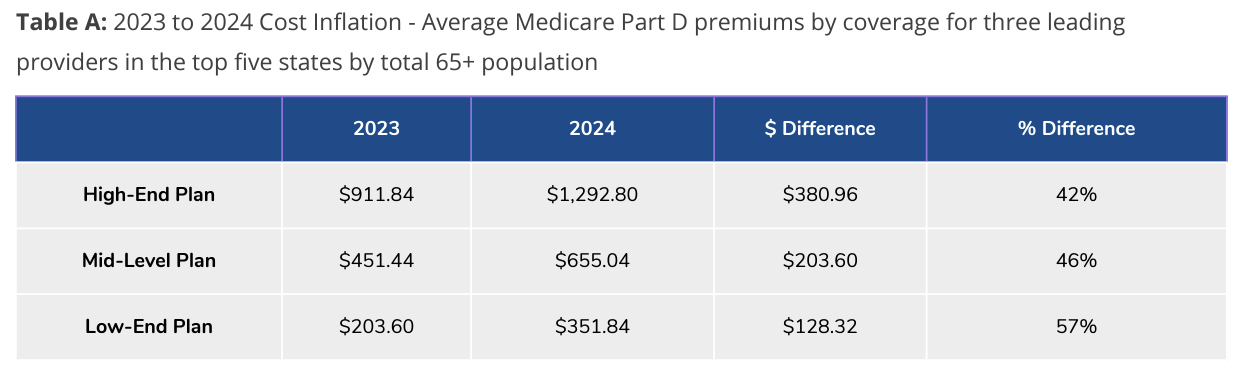

In five states with the largest populations over age 65 – California, Florida, New York, Pennsylvania, and Texas – the cost of average premiums is projected to rise dramatically. According to HealthView Services, premiums are expected to surge between 42% and 57% in 2024.

The Inflation Reduction Act, signed into law in August of 2022, introduces significant changes to prescription drug costs under Medicare and Medicare Advantage plans. One key provision is the reduction in the maximum annual out-of-pocket spending on prescription drugs, which will be lowered to $2,000 in 2025. This change is expected to shift more responsibility for catastrophic coverage onto Part D plan providers, potentially contributing to higher premiums in the short term.

Today, the federal government covers 80% of the costs above the maximum out-of-pocket limit for Part D drugs, while insurers cover the remaining 20%. With the new cap coming in 2025, insurers will be responsible for 60% to 80% of these costs, leading to higher premiums for beneficiaries.

Social Security COLA and Medicare Costs

Retirees will receive a small Social Security cost-of-living adjustment (COLA) in 2024 – 3.2% compared to 8.7% in 2023. This increase may not suffice to cover the rising Medicare costs, particularly for those on high-end Part D plans. For instance, 54% of the COLA may go towards covering additional Part D premium costs.

Pros and Cons for Medicare Users

Pros

- Long-Term Savings: The Inflation Reduction Act’s cap on out-of-pocket costs, starting in 2025, promises significant long-term savings for beneficiaries.

- Enhanced Coverage: The increased premiums could lead to improved coverage options and access to a broader range of medications.

Cons

- Immediate Financial Burden: The sharp increase in premiums places an immediate financial strain on retirees, especially those with fixed incomes.

- Reduced Social Security COLA Impact: With higher Part D premiums, the effectiveness of Social Security COLA increase is diminished, affecting retirees’ purchasing power.

Impact on Local Government with OPEB Plans

Liabilities for OPEB plans are primarily influenced by the cost of coverage, with prescription drug expenses playing a significant role. Higher premiums in turn elevate the OPEB liabilities reported in financial statements. This results in increased annual expenses for both the organization and retirees, exerting additional pressure on other budgetary areas.

Pros

- Potential for Long-term Cost Control: The cap on out-of-pocket expenses could stabilize or even reduce the long-term healthcare liability for these plans.

- Opportunity for Plan Optimization: The changes necessitate a review of existing OPEB plans, providing an opportunity to optimize and streamline retiree healthcare benefits.

Cons:

- Immediate Increase in Liabilities: The immediate spike in premiums may increase the short-term financial burden on local governments, potentially impacting their budgets and fiscal planning.

- Administrative Challenges: Adapting to these changes requires administrative effort and may lead to complexities in managing OPEB plan provisions and communications with retirees.

In Summary

The increase in Medicare Part D premiums in 2024 presents both challenges and opportunities for individual beneficiaries and local governments. By understanding these changes, both groups can make informed decisions and adjustments to their strategies. For Medicare users, it’s about managing immediate costs while anticipating future savings. For local governments, it involves balancing short-term financial pressures with long-term fiscal responsibility. In both cases, proactive planning and informed decision-making will be key to navigating these changes successfully.

If you have any questions on this, please reach out to one of our Odyssey consultants. If you’d like to receive news like this straight to your inbox, please subscribe to our newsletter above.

Categories:

Share