How Much Does it Cost to Start a 401(k) Plan?

Bottom Line Up Front

- Setting up a 401(k) plan is affordable for small businesses, with initial costs ranging from $500 to $2,500 and the SECURE Act providing substantial tax credits.

- Ongoing administration fees vary, and many businesses benefit from using a third-party administrator.

- Offering a 401(k) plan is an effective tool for attracting and retaining employees, providing them and the business significant tax advantages and financial growth opportunities.

As a small business owner, you might be curious about the expenses associated with offering a 401(k) plan to your employees. You might have even dismissed the idea, assuming that 401(k) plans are exclusively for larger companies due to their perceived high costs. However, this is not accurate. The cost of a 401(k) plan can vary significantly based on factors such as company size, plan complexity, investment choices, and associated fees. Today, many 401(k) plans are quite affordable. In this article, we will delve into the specifics of these costs.

You can use our guide to a 401(k) plan to learn more about these plans and how they can greatly benefit you and your employees.

Please note that the information provided in this article is not intended as legal advice or a comprehensive interpretation of ERISA or any other applicable laws. It should not be misconstrued as financial or investment advice. Always consult with a qualified professional for legal, financial, and investment guidance specific to your circumstances.

Initial 401(k) Set-Up Costs

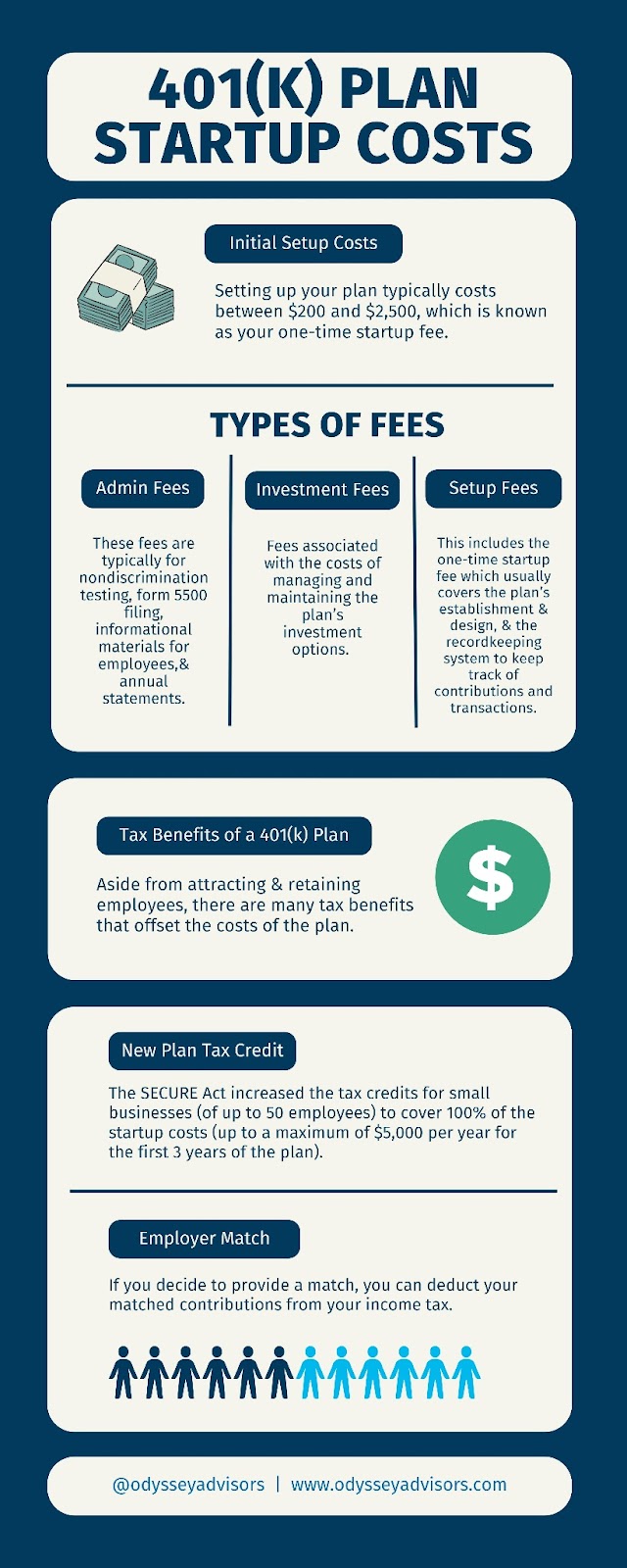

Setting up your 401(k) plan typically costs between $500 and $2,500, which is known as your one-time startup fee. These fees cover the cost of working with a retirement plan specialist in order to design the plan. Other costs associated with the plan’s set-up are establishing a recordkeeping system to keep track of contributions and transactions. You will also need to provide educational materials to help employees understand the features of the new 401(k) plan.

However, there is a tax credit available to small companies that are initially starting a 401(k) plan:

- When the SECURE Act 2.0 was signed into law, it included enhanced tax credits for small businesses of up to 50 employees who are starting a new 401(k) plan. However, it does phase out for businesses with 51 to 100 employees.

- You can also earn an additional $500 tax credit by adding an automatic enrollment feature to a new or existing 401(k) plan which is available for the first three years the feature is effective.

Now if combined, these credits can total up to $5,500 per year for a total of up to $16,500 for 3 years.

401(k) Plan Administration Fees

401(k) plan administration involves annual fees paid to the plan administrator for managing the plan effectively unless you plan to handle these on your own. Many small businesses choose to hire a third-party administrator (TPA) to handle the day-to-day administration.

These administrators play a crucial role in maintaining your plan’s smooth operation. They handle various tasks, including recording participant contributions, managing investment choices, processing transactions, and conducting compliance testing to ensure the plan adheres to legal requirements. Additionally, administrators prepare annual statements, such as the Form 5500, and provide assistance for plan-related inquiries.

Many of the plan administration fees come from:

- Nondiscrimination testing

- Form 5500

- Informational materials for employees

- Annual statements

The fees charged by third-party administrators can vary based on the plan’s size and complexity but typically fall within the range of $1,750 to $5,000 per year.

Employer Match Contribution Costs

You can also contribute a percentage of employee’s contributions to the plan. For example, an employer might match each dollar of the employee’s contribution up to 5% of their pay. Therefore if the employee earns $100,000 and contributes $5,000, then the employer will also contribute $5,000.

Although there is no law requiring employers to match employee contributions, most do as it is a way to build goodwill and loyalty with their employees. Another reason employers often contribute to the plan is to reduce taxes. Employers can deduct matched contributions from their income taxes. However, the IRS sets contribution limits each year for how much employees may contribute. For 2024, the 401(k) limit is $23,000.

Investment Fees

Investment fees are typically associated with the costs of managing and maintaining the investment options offered within the plan. Different investment options in the plan will have an expense ratio, which represents the percentage of assets deducted each year to cover operating expenses.

There are other potential fees depending on the features of the plan, typically with more complex plans having higher fees. These fees are not typically paid by the employer, however as the employer your choice for plan asset provider will influence the fees employees will have to pay.

Tax Benefits of Starting a 401(k)

So while a 401(k) plan is an investment, many small businesses are choosing to make the switch for the plethora of benefits. Aside from attracting and retaining employees, there are many tax benefits that can offset the total costs of the plan.

The SECURE Act, passed in late 2019, increased the tax credits for small businesses (of up to 50 employees) to cover 100% of qualified start-up costs (up to a maximum of $5,000 per year for the first three years of the plan).

And, as mentioned above, if you offer an employee match contribution, any match you make is tax-deductible.

If you’re interested in learning more about how to get started, check out this step-by-step guide to starting a 401(k) plan.

In Summary

Long story short, offering a 401(k) plan is not only feasible for small businesses but also comes with several financial benefits. With the initial setup ranging from $500 to $2,500, and the SECURE Act providing substantial tax credits, especially for businesses with up to 50 employees.

If you’re looking to contribute more to your retirement plan, a 401(k) is the way to go. In fact, 401(k) plans offer the flexibility to contribute significantly more than other retirement plans. For an in-depth look at how you can maximize your contributions, especially through advanced techniques like cross-testing, read our article on 401(k) Cross-Testing.

As a specialized third-party administrator, we provide comprehensive services to streamline the setup and management of your 401(k) plan. Our expertise ensures compliance, efficiency, and maximized benefits for you and your business, allowing you to focus on growth while offering a valuable employee benefit. By partnering with us, you can leverage the full potential of a 401(k) plan without the administrative complexities.

Contact us today to learn how we can help you provide retirement benefits for your employees and stay ahead of the curve.

About The Author Luke graduated from the University of Connecticut with a B.A. in Actuarial Science. He brings a strong mathematical and analytical background to his role as a Consulting Actuary at Odyssey Advisors. He designs and maintains complex client-employee benefit programs...

More Insights From This author