Step-by-Step Guide to Starting a 401(k) Plan

Bottom Line Up Front

- A 401(k) plan can provide many benefits to both you and your employees, such as tax savings, retirement savings, and the potential for employer-matching contributions.

- To start a 401(k) plan, you’ll need to find a provider, determine which plan would best fit you and your employees’ needs, establish a plan document, onboard your employees, and establish a set of procedures in order to keep the plan running smoothly.

- A TPA is a company that specializes in qualified plan administration and they can help set up your plan and perform a number of the day-to-day administrative tasks of running a plan.

What are 401(k) plans?

401(k) plans are a type of retirement savings plan that’s offered by many employers. It’s named after the section of the Internal Revenue Code that defines it. 401(k) plans allow employees to save and invest a portion of their income for retirement on a tax-deferred basis. This means that the employee does not pay taxes on the money that they contribute to the plan until they withdraw it in retirement. Many 401(k) plans also offer employer matching contributions, which can help employees save even more for retirement. Additionally, many 401(k) plans offer a Roth option whereby employees contribute on an after-tax basis but all earnings will be tax-free upon retirement.

The Benefits of Starting a 401(k) Plan For Your Business

Many employers offer different benefit programs to attract and retain talent. The benefits they offer ensure their employees feel valued and help them build financial security. It has become standard practice for a business to offer a 401(k) plan which means those that aren’t currently offering a similar plan, can be seen as lacking.

There are also tax benefits for sponsoring a 401(k) plan. Employer contributions to the plan are deducted from the employer’s federal tax return, as long as they do not exceed IRC limitations. Elective deferrals and investment gains are also not currently taxed and enjoy tax deferral until distribution.

When the SECURE 2.0 Act was signed into law, it included enhanced tax credits for small businesses (up to 50 employees) that start a new 401(k) plan. The new credit allows you to claim a tax credit of 100% of the startup costs (capped at $5,000 per employer per year for three years). However, it does phase out for businesses with 51 to 100 employees.

You can also earn an additional $500 tax credit by adding an automatic enrollment feature to a new or existing 401(k) plan which is available for the first three years the feature is effective.

Now if combined, these credits can total up to $5,500 per year for a total of up to $16,500 for 3 years.

How to Start a 401(k) Plan for a Small Business?

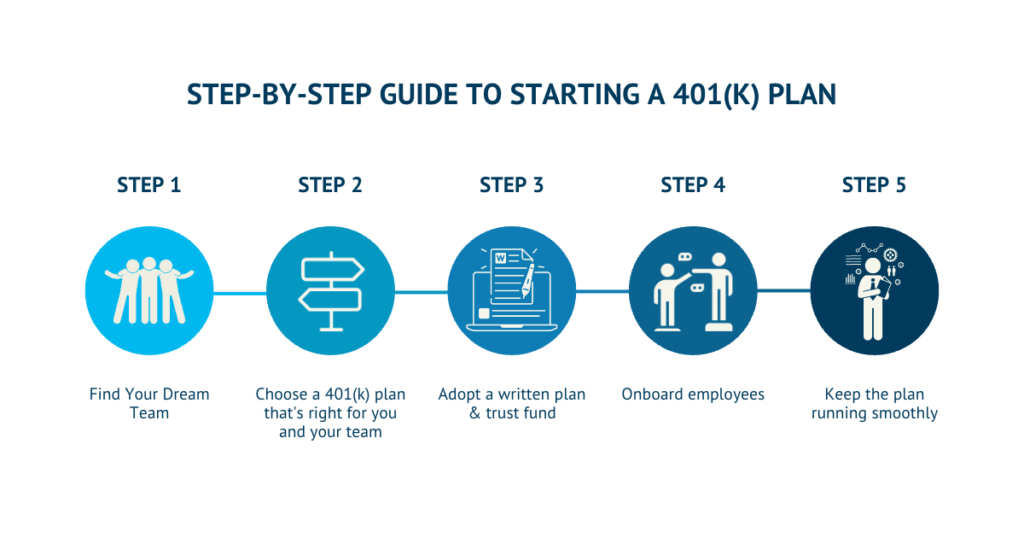

To start a 401(k) plan for your business, there are 5 steps you’ll need to take.

The IRS covers the initial steps, but if you’d rather not wade through it, here’s an easier step-by-step guide.

- Find Your Team

- Choose a 401(k) Plan That’s Right for You and Your Team

- Adopt a Written Plan & Trust Fund

- Onboard Employees

- Keep the Plan Running Smoothly

Working with an expert, they can provide guidance in order to design the best plan to suit your business’s needs.

Step 1: Find Your Team

This part is highly important when starting a 401(k) plan. You’ll want to do some research to find the best firms that provide recordkeeping and third-party administration (TPA) services for 401(k) plans. Focus on providers that can serve you and your employees long-term with extensive resources and excellent customer service.

What Should I Look For in a 401(k) Provider?

When choosing a 401(k) provider for your business, there are several factors you should consider. Some of the most important include the provider’s reputation and track record, the fees and expenses associated with the plan, the investment options offered, the level of customer service and support provided, and the flexibility of the plan. You should also consider whether the provider offers any additional services, such as financial planning or educational resources, that could be beneficial to your employees. It is a good idea to compare the features and costs of different providers before making a decision.

Here’s why you might want a TPA and how to hire the right one

Step 2: Choose Which 401(k) Plan Is Right for You and Your Team

Once you’ve found a provider, it’s time to figure out which plans fit both your business’s and your employee’s needs. This is where your provider can start to guide you in the right direction based on their experience with companies similar to yours if you’re unsure. It’s also important to do your own research as well. Here are a few 401(k) plan options available to businesses regardless of size:

- Traditional 401(k) plan: this is the most flexible option because employers can decide when, how, and if they want to make contributions to employee accounts. Bear in mind, that these plans are subject to annual IRS nondiscrimination testing.

- Safe Harbor 401(k) plan: this plan is similar to a traditional 401(k), but requires that employers contribute to their employees’ accounts that are fully vested when made. There are also specific rules regarding how contributions need to be structured. However, these plans have a safe harbor status which means they are exempt from some annual IRS non-discrimination tests while standard plans must pass these tests each year.

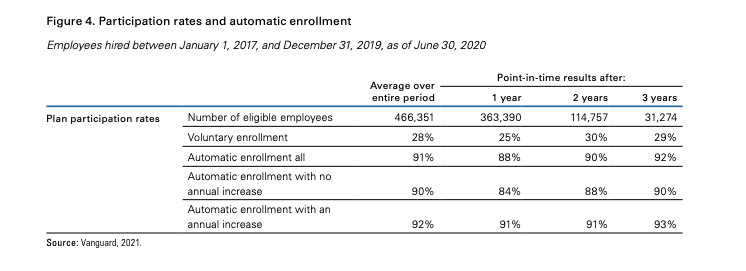

- Automatic enrollment 401(k) plan: This plan allows you to automatically enroll employees and place deductions from their salaries in certain default investments unless employees elect otherwise. Employers may choose this option as a way to increase participation in their 401(k) plans. Contributions to this plan qualify as elective deferrals.

According to one of the largest 401(k) providers, Vanguard Group, 92% of new hires were still contributing to their 401(k) plan three years after being automatically enrolled and for those with voluntary enrollment, only 29% were still saving.

Step 3: Adopt a Written Plan & Trust Fund

Once you’ve determined what plan you’ll be using, you’ll need to create a written document that serves as the foundation for day-to-day plan operations. If you choose to hire a TPA or plan administrator, they will typically take care of creating this document. You’ll want to make sure the following items are included in your plan document:

- Description of benefits & features of the plan

- Employee eligibility

- Summary Plan Description (SPD)

- Vesting schedule (if needed)

- Contact information for all parties involved with the plan

- Distribution management

- Any additional details such as employer matching, profit sharing, etc.

Setting up a Trust Fund for Plan Assets

The plan’s assets are required to be held in a trust to ensure that they are only used for the benefit of plan participants and their beneficiaries. You also need to determine a trustee to handle the contributions, plan investments, and distributions to and from the plan.

Step 4: Employee Onboarding

Once the plan is starting to come together, you must notify all eligible employees about the plan benefits and requirements. You’ll need to do this about 30 days in advance. This is where a summary plan description (SPD) would come into play. An SPD is a primary way to share information about the plan and how it operates with eligible employees and their beneficiaries. In addition, you may want to share the benefits/perks of joining your 401(k) plan.

Holding an all-hands meeting to go over the new plan and allow for an open Q&A can help your employees get a better understanding of the new plan. Some common questions plan participants may ask about the new plan:

- Will there be an employer match?

- What types of plans are available and what are their features?

- Is there a minimum/maximum I can contribute to the plan?

- How do I set it up?

- What’s the vesting schedule look like?

- What are the investment options & can we select our own?

- Am I required to enroll in the company’s plan?

- At what age do payouts begin/when are we required to start taking payouts?

- Are we allowed to borrow from the account and if so, are there any penalties or restrictions?

Step 5: Keep the Plan Running Smoothly

Annual Nondiscrimination Testing

The IRS requires that certain retirement plans perform a non-discrimination test every year. These tests are used to determine if the plan is disproportionately benefiting highly compensated employees (HCEs) over non-highly compensated employees (NHCEs). If the plan fails these tests it can lose the tax deductions it receives for any contributions made to the plan.

Disclosing Plan Information to Participants

As mentioned above, there are certain documents that must be disclosed to the plan’s participants in order to keep them informed about the basics of the plan, make them aware of any changes, and allow them to make any decisions or changes in a timely manner.

There are 6 different notices that should go out as needed:

- The summary plan description (SPD) is a basic descriptive document geared towards the plan’s participants that explains the plan’s features and what to expect from the plan. It can also include information regarding when and how to become eligible to participate, the vesting schedule, how to file a claim for the benefits, etc.

- A summary of material modification (SMM) notifies participants of any changes that are made to the plan or the information that is included in the SPD.

- An individual benefit statement (IBS) is a statement you must provide participants with information about their account balances and benefits.

- A summary annual report (SAR) is a one-page summary of the important information from your Form 5500 and the plan’s finances that get distributed to the plan’s participants. This form is required by ERISA to be distributed annually and if/when a plan participant requests it.

- A blackout period notice gives participants an advance notice of when a blackout period will occur. A blackout period is a time when participants won’t be able to access their 401(k) accounts because a major plan change is being made. If the blackout is going to last for more than three days, you must provide the notice. It must be sent at least 30 days out, but no more than 60 days out from the start of the blackout.

Government Reporting

In addition to compliance testing, the IRS and Department of Labor (DOL) require you to file an annual report which discloses plan information and its operation. The main form used for this is Form 5500.

Recordkeeping

You’ll also need to develop a recordkeeping system. This system will help you keep track of earnings and losses, plan investments, expense, and benefit distributions in participants’ accounts. The investment provider will usually provide these recordkeeping services in combination with your TPA.

This system will also help you prepare for your annual return/report that must be filed with the Federal government.

The Best Time to Start a 401(k) Plan

The best time to start a 401(k) plan for your business is as soon as possible. This is because a 401(k) plan can provide many benefits to both you and your employees, such as tax savings, retirement savings, and the potential for employer-matching contributions. Additionally, establishing a plan can help you attract and retain talented employees by offering a valuable benefit. While there may be some initial costs and administrative tasks involved in setting up a 401(k) plan, the long-term benefits can make it well worth the effort.

Starting a 401(k) Plan Doesn’t Need to Be Overwhelming

Starting a new 401(k) plan will take some time and preparation and it can be overwhelming when you see everything laid out like above. But it doesn’t have to be. Once the above decisions are made, you can work with a TPA who can guide you through the entire process and take on the administrative tasks.

At Odyssey Advisors, we can help you cut through the complexity, make informed and strategic decisions, and design a plan that is tailored to meet both your personal and professional needs. If interested, you can schedule a no strings attached consultation with one of our TPA specialists here. Seriously, no strings.

And if you’re looking to terminate a 401(k) plan, take a look at our guide here.

About The Author Stephanie joined the Odyssey Advisor’s team all the way from the Lonestar state in November of 2020. She is versatile in her abilities and has experience in copywriting, photography, and analytics. She helps tell our brand story and convey...

More Insights From This author

Explore More Resources