How Your OPEB Long-Term Rate of Return Is Determined

Bottom Line Up Front

- The long-term rate of return is the expected average income and capital appreciation for a municipality’s investments over the lifetime of all currently active and retired plan members.

- An actuary’s long-term rate of return assumption is based on a review of the investment policy (mix of investments), expected inflation rate, expected return on various asset classes, and the expected investment expense.

- Actuaries are required to do an independent review of the return assumptions used by investment advisors which is why their rates may differ.

This article will help you understand how actuaries determine and utilize a key assumption, the expected long-term rate of return on OPEB assets. With more and more emphasis being given to the funded status of OPEB plans, understanding this key input into an OPEB plan has never been more important.

Long-Term Rate of Return and Why It Matters

The long-term rate of return is the expected average income and capital appreciation for a municipality’s investments over the lifetime of all currently active and retired plan members.

The long-term rate of return on assets is an important assumption in a GASB 74/75 report. The GASB 74/75 standards specify that the discount rate used to determine the present value of a municipality’s OPEB liability is based on the long-term rate of return on assets and a 20-year high-grade Municipal Bond Index. Whether the discount rate is based on the bond or asset rate of return depends on the funded status of the plan, future contributions and benefit payments, as well as the investment policy and anticipated future contributions (funding policy). So, plans that are better funded get to use a higher discount rate versus those that aren’t funding at all.

Top 5 factors that determine your OPEB discount rate

Why Doesn’t The Assumed Rate of Return From My Actuary Match My Investment Advisor’s Projected Return?

Your actuary must perform an independent evaluation of expected investment returns. Additionally, GASB 74/75 requires us to use specific methods when projecting expected returns. Both of these factors, and several others, may cause a different investment return assumption between your actuary and your investment advisors.

Our 5 Step Process Used to Determine The Long-Term Rate of Return

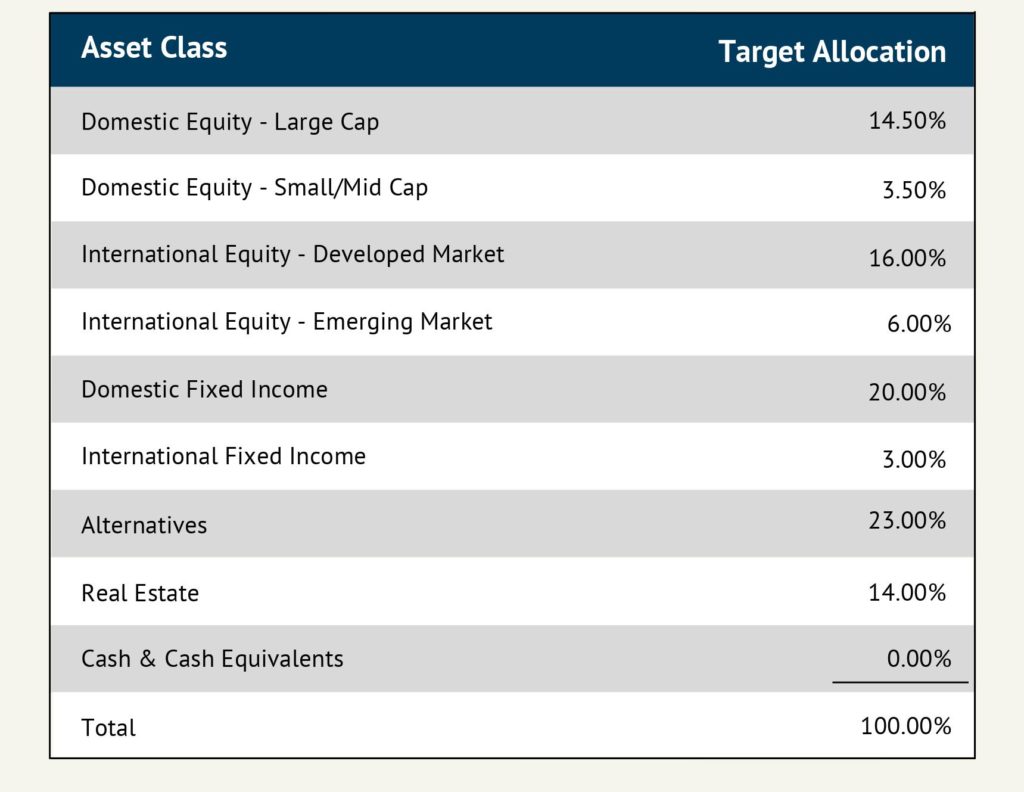

- The first thing we do is look at the investment mix or formal investment policy.

Is the plan invested in stocks, bonds, real estate, alternative investments (i.e. commodities, private equity, hedge funds, etc.), and/or cash? Are the stocks or bonds domestic or international? Large-cap or small/mid-cap? The big question is what percentage of the portfolio is invested in each of these different asset classes. For example, let’s use the asset mix below:

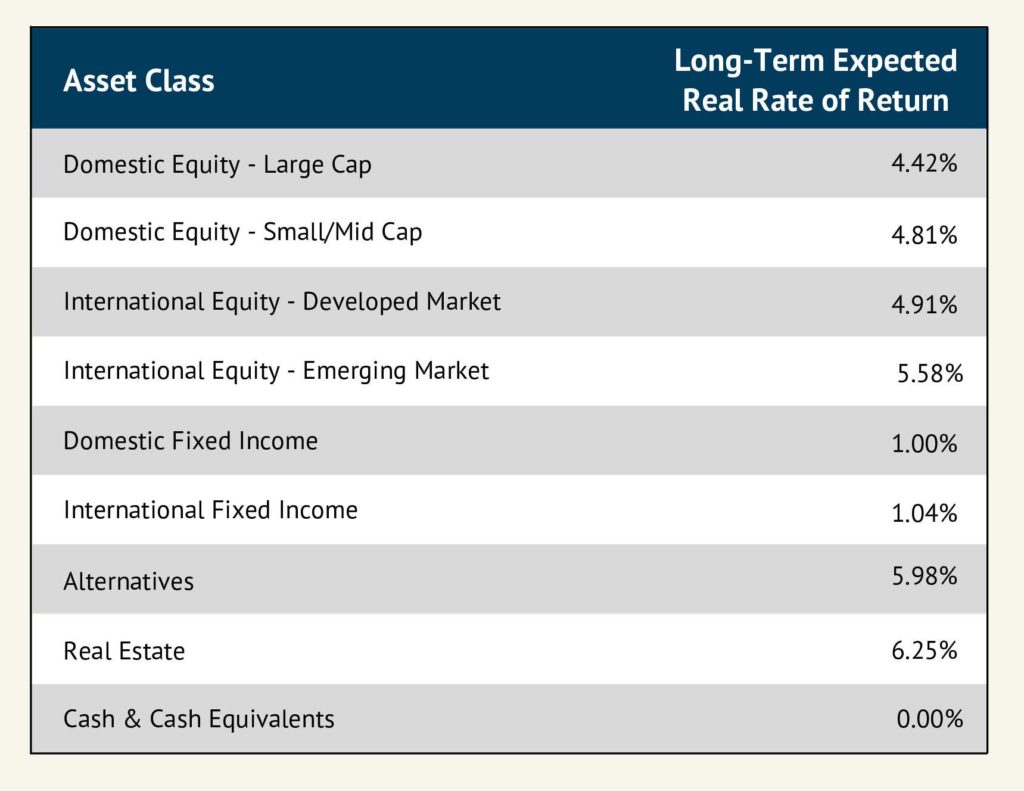

- Now that we know the mix of assets, we can begin determining the expected return for each asset class.

GASB requires that actuaries use a “building block” approach. This means that we start with an expected inflation rate, let’s say 2.50%, and “build” or add an expected excess return over inflation for each asset class.

- From that inflation “building block” we have to determine the excess expected return over inflation for each asset class.

There are several ways to do this. Many asset managers will provide their expected portfolio return, the actuary may decide to use their numbers or not. On the other hand, the actuary may do their own study of historical returns on investments using that as the basis for expected returns. At Odyssey Advisors, we use a survey of financial consultants and their long-term expected returns by asset class. Below is an example of an expected return by asset:

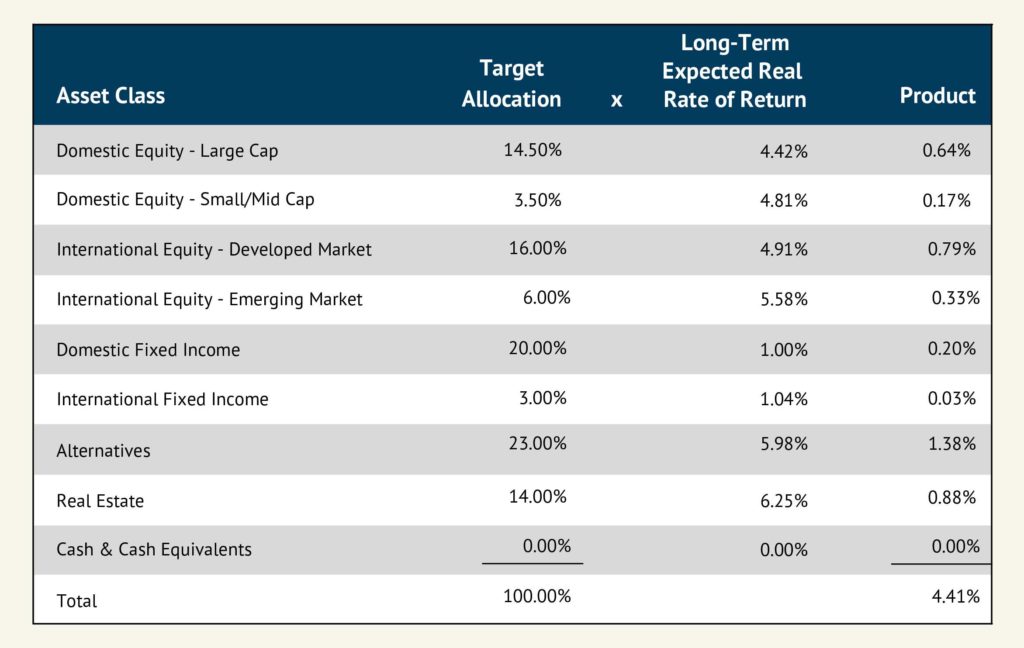

- Next, we determine the expected total return using the expected return for each asset class and the percentage of the portfolio allocated to each asset class.

We multiply the Target Allocation by the Expected Return for each asset class, then add all those products together (this is also called a “weighted average”), as shown below:

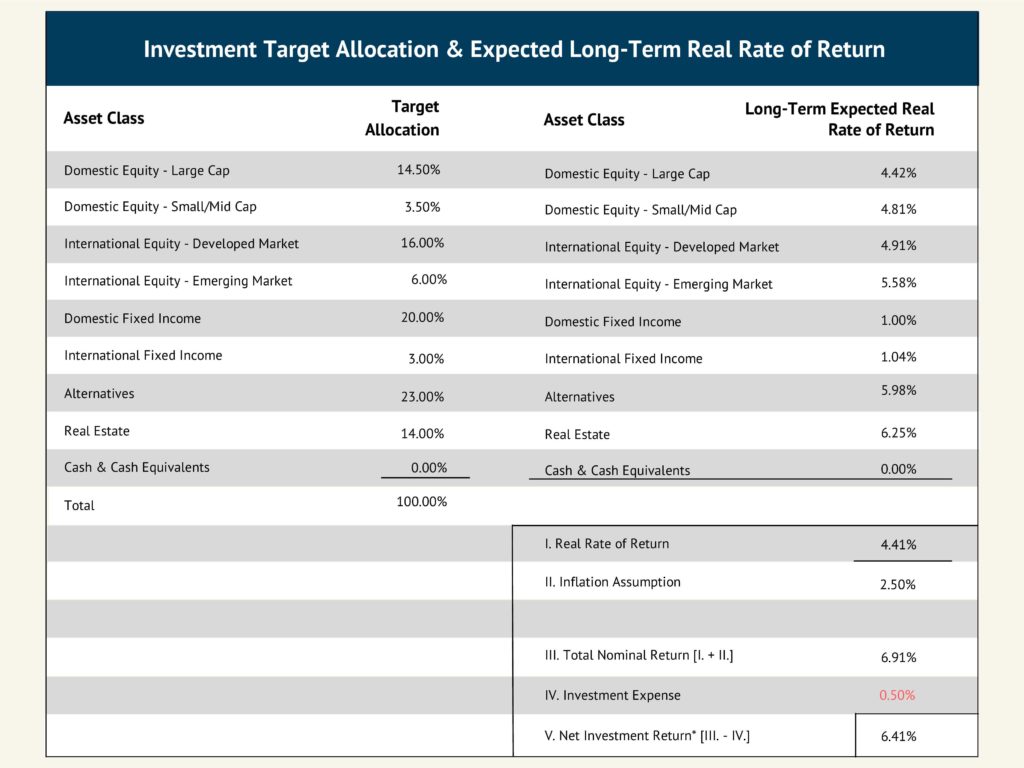

Here’s how the GASB 75 investment rate of return is determined

- Add the inflation back in and subtract the assumed annual investment expenses:

Using this methodology, our portfolio creates an expected long-term return of 6.41%.

In Summary

Your actuary is required to do an independent review of the asset return assumptions so don’t be surprised if they differ from those of your investment advisor. The actuary’s long-term rate of return will be based on a review of the mix of investments, expected inflation rate, expected return on various asset classes, and the expected investment expenses. Who would have guessed that so many factors went into just one actuarial assumption!

Check out this video on the key assumptions that affect your OPEB liability.

If you still have questions or would like a free review of your latest valuation, you can reach me or one of my fellow colleagues here.

Whenever you’re ready, there are 3 ways we can help you:

About The Author Kurtis has been a consultant on the Odyssey Advisors team since 2013 and has developed extensive knowledge and expertise in developing and administering retirement benefit solutions. Kurtis is passionate about helping people achieve the retirement they’ve always dreamed of...

More Insights From This author

Explore More Resources