Understanding the Impact of Inflation on OPEB Liabilities

Bottom Line Up Front

- Rising inflation drives up healthcare costs, increasing your OPEB liability.

- Inflation-driven interest rate changes may partially offset liability increases, depending on your plan’s funding status.

- You can better manage inflation risk by pre-funding OPEB obligations.

Other Post-Employment Benefits (OPEB) liabilities represent the projected future costs of benefits promised to your retired employees, with retiree healthcare expenses typically making up the largest share. Because these obligations often span decades, it’s critical to understand how inflation influences them.

Inflation affects OPEB liabilities in two main ways:

- Healthcare costs – higher inflation often means faster growth in medical expenses.

- Discount rates – rising rates can temporarily offset liabilities, depending on your funding status.

In this article, I’ll walk you through how inflation impacts these two key assumptions and what that means for your OPEB liabilities.

Medical Cost Trends

Medical care cost inflation is the assumption used to project the future growth of healthcare expenses (physician fees, prescriptions, medical services). Since retiree medical costs are often the largest component of OPEB, higher premiums directly lead to higher liabilities.

Real-World Example: Post-COVID Surge

After the COVID-19 pandemic, we saw a spike in healthcare costs as people returned for procedures that they deferred, as well as healthcare providers looking to make up for lost earnings during a period of higher inflation. As a result, many actuaries (including myself) updated our assumptions to better reflect short-term spikes before projecting smaller, steadier increases later.

As of 2021, actuaries now rely on the Getzen Healthcare Cost Trend Model, which links medical costs to long-term economic growth while accounting for short-term shocks like COVID.

This Getzen Model incorporates assumptions about economic growth (GDP per capita), long-term healthcare cost growth, and a gradually declining “excess cost growth” factor that reflects how much faster healthcare costs are expected to rise compared to the overall economy.

By applying this framework and adjusting short-term assumptions to account for elevated cost pressures in the early 2020s, most actuaries developed annual trend rates that started higher but eventually settled back into more sustainable, economically aligned growth.

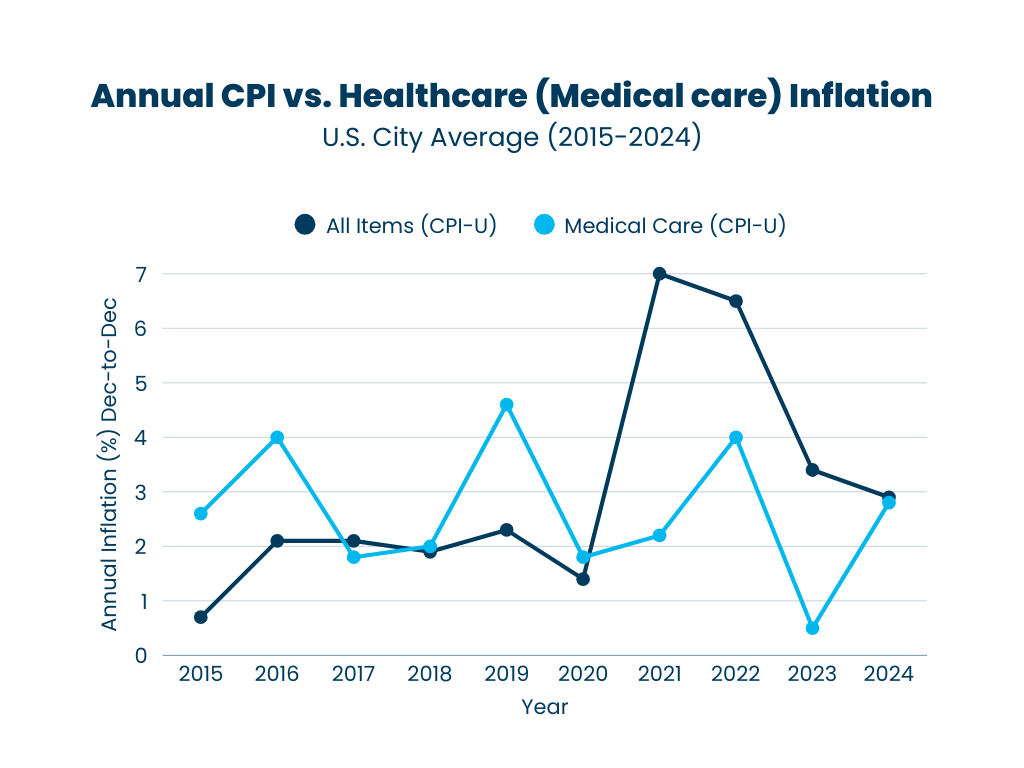

The Unique Drives of Medical Cost Growth

As you can see in the graph above, general inflation and medical care inflation are not perfectly correlated because a variety of additional factors drive healthcare cost growth beyond overall price changes in the economy, including but not limited to:

- Cost shifting plays a significant role: when government programs reimburse providers at lower rates, a greater share of costs is often shifted to private insurers. Similarly, employers often pass on rising healthcare expenses to employees through higher premiums, deductibles, and out-of-pocket maximums, often in exchange for more affordable plans or Health Savings Accounts.

- Certain government mandates, including required coverage of certain benefits and regulatory changes, can increase the cost of providing care and insurance.

- Uncompensated care from uninsured or underinsured patients also further raises costs, as providers often offset these losses by charging higher prices to insured populations.

- Advances in medical technology and the introduction of new treatments, while improving outcomes, often come with a premium, especially with costly specialty drugs and procedures.

- Demographic changes, such as an aging population and rising rates of chronic conditions, also contribute to increased demand for healthcare services.

Together, these factors place sustained upward pressure on healthcare costs, often outpacing general inflation over the long term.

How Inflation Affects Discount Rates

The two key rates used in the discount rate calculation are the 20-year municipal bond index rate and the long-term rate of return on plan assets. Your plan’s funding status determines how these rates are applied:

- Fully funded plans – the discount rate equals the expected long-term rate of return (inflation plus the long-term return).

- Partially funded plans – the discount rate will be a blended rate equivalent to discounting all expected future benefit payments that may be funded by assets held in the OPEB Trust at the expected long-term rate of return, with all other payments discounted using the 20-year index of yields on high-grade municipal bonds. (Most plans fall into this category.)

- Unfunded plans – the discount rate will be the 20-year index of yields on high-grade municipal bonds.

When inflation rises, municipal bond yields usually rise as well. For underfunded plans, this may lead to a reduction in your disclosed Total OPEB Liability (TOL) due to a higher discount rate being applied. But keep in mind: historically, elevated inflation in the U.S. has been short-lived. So while your liabilities may temporarily decline, that effect could reverse as inflation and rates settle back down.

Inflation rates also influence financial markets. During high-inflation periods, certain sectors may see declining equity prices, which can negatively impact overall portfolio performance. Depending on the composition of the investments in your OPEB Trust, you may realize lower returns during these periods of high inflation. For fully funded plans, those reduced returns could lead to a downward adjustment in the discount rate, which may increase your TOL.

For partially funded plans, higher inflation may boost the municipal bond rate, which can raise the blended discount rate and reduce liabilities. However, if inflation depresses asset returns or shortens the period during which assets can cover benefits, that benefit could be offset or even erased.

The discount rate for a funded OPEB plan is generally less volatile compared to that of an unfunded plan, which relies solely on the municipal bond rate. That’s why establishing and maintaining funding remains the most effective strategy for you to manage long-term OPEB obligations.

Read more: Selecting the Best Funding Strategy for Your OPEB Trust

Key Takeaways

Inflation impacts your OPEB liability, mainly through its effect on two assumptions:

- Medical cost trend rates – periods of high inflation often result in short-term spikes in healthcare costs.

- Discount rates – rising bond rates may temporarily reduce liabilities in unfunded plans, while funded plans could see liabilities rise if investment returns suffer.

Although there is no way to completely shield your plan from the effects of inflation, staying informed about economic trends will allow you to anticipate potential changes. Regularly updating actuarial assumptions and implementing sound funding strategies can help mitigate inflation’s impact and help prepare you for any financial challenges that come your way.

At Odyssey Advisors, we’re here to support you in navigating these complex challenges. Please don’t hesitate to contact us if you have questions or want guidance tailored to your needs.

About The Author Luke graduated from the University of Connecticut with a B.A. in Actuarial Science. He brings a strong mathematical and analytical background to his role as a Consulting Actuary at Odyssey Advisors. He designs and maintains complex client-employee benefit programs...

More Insights From This author

Explore More Resources