Top 5 Factors that Determine Your OPEB Discount Rate

KEY POINTS

- Per GASB Statement 75, government entities that sponsor Other Postemployment Benefits (OPEB) Plans are required to get a valuation done at least every other year.

- In order to determine your Total OPEB Liability (TOL), an actuary will establish a discount rate that will apply to all future expected benefits payments.

As a government entity that sponsors an Other Postemployment Benefits (OPEB) Plan, you’re required to have an actuary perform a valuation, at a minimum, every other year. Part of the valuation requires your actuary to determine a specific discount rate which is used to calculate your Total OPEB Liability (TOL).

What is an OPEB Plan?

OPEB plans offer benefits to former or retired employees that aren’t pensions. These benefits are primarily healthcare benefits but often will also include dental insurance, life insurance, and other ancillary benefits. You are required to have an actuary to value these benefits for financial statement reporting, but they can also provide consulting services regarding plan design, pre-funding benefits, etc.

How is the discount rate calculated?

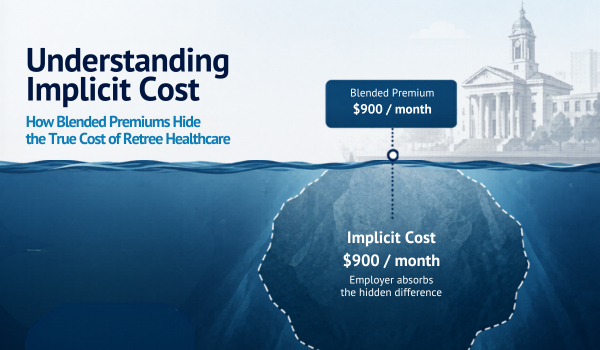

Two key rates are used in the calculation – the 20-year municipal bond index rate and the long-term rate of return on plan assets. For most plan sponsors, the discount rate will be a blend of those two figures. There are three funding scenarios that will determine the discount rate:

- Fully funded plans – the discount rate will be the expected long-term rate of return (sum of inflation and the long-term real rate of return)

- Partially funded plans – the discount rate will be a blended rate equivalent to discounting all expected future benefits payments that may be funded by assets held in the OPEB Trust at the expected long-term rate of return with all other payments discounted using the 20-year index of yields on high-grade municipal bonds.

- Unfunded plans – the discount rate will be the 20-year index of yields on high-grade municipal bonds.

Top 5 factors an actuary uses to determine the discount rate used to calculate the Total OPEB Liability (“TOL”)

- The current level of assets held in the OPEB Trust. This is normally found on the OPEB Trust statement. A higher level of assets to current and future expected benefit payments will place more weight on the expected long-term real rate of return and less on the 20-year index of yields on high-grade municipal bonds.

- Expected future benefit payments. This is dependent on a variety of other assumptions including but not limited to:

- Current benefit payments

- Demographics

- Healthcare inflation

- Retiree contribution rate

- Integration with Medicare

- Expected future contributions to the OPEB Trust by the plan sponsor. This is the formal policy of the plan sponsor to contribute to the OPEB Plan. Some entities have a statutory contribution obligation but for most this is a policy adopted by the municipal organization.

- Absent a formal policy, the actuary will review the average of the OPEB Trust contributions for the prior five (5) years to forecast future contributions.

- Absent a formal policy, the actuary will review the average of the OPEB Trust contributions for the prior five (5) years to forecast future contributions.

- The asset allocation of funds held in the OPEB Trust and the expected long-term real rate of return by asset class. The actuary seeks to forecast real rates of returns by asset class (e.g., large-cap growth equities, domestic bonds, private equity, etc.) and applies those to the target asset allocations for each asset class to determine the expected real rate of return for the portfolio. The actuary may seek guidance on this from the plan’s investment professionals, and use survey data or other methods as appropriate.

- The 20-year index of yields on high-grade municipal bonds. This index changes daily and is subject to large swings so an unfunded plan is likely to see a volatile Total OPEB Liability from period to period. There are several sources for this index with Standards & Poor’s and Bond Buyer being two of the most prevalent.

This is not meant to be an exhaustive list of actuarial assumptions as some actuaries make more or less depending on the size of the group and the purpose of the valuation.

Whenever you’re ready, there are 3 ways we can help you:

About The Author As President and CEO of Odyssey Advisors, Parker Elmore is dedicated to quality service, expertise, and efficiency. With over 35 years of industry experience, Parker and the Odyssey team develop and implement solutions to the complex financial issues faced by...

More Insights From This author

Explore More Resources