Required Minimum Distributions (RMDs): When to Start Planning

Bottom Line Up Front

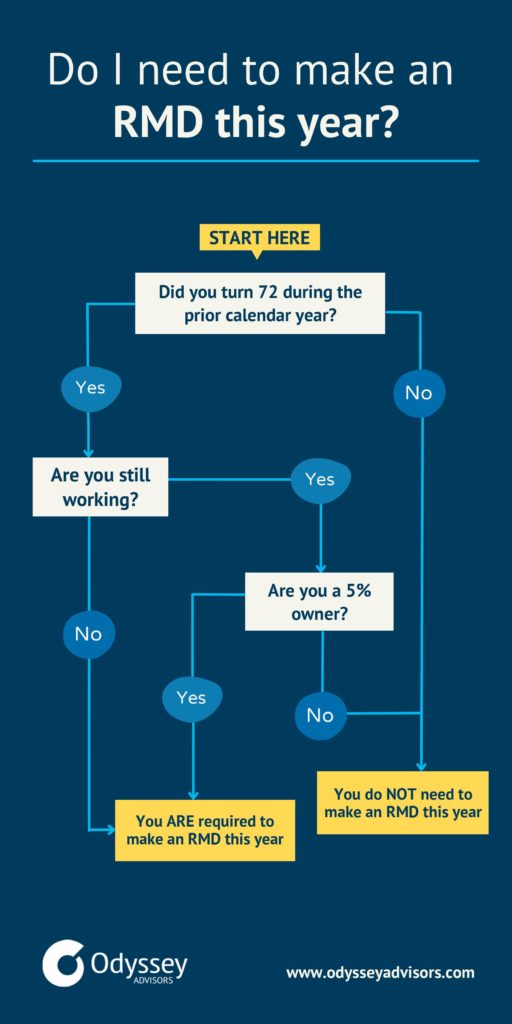

- Under current law, you’re required to start making withdrawals known as Required Minimum Distributions (RMDs) from your tax-deferred retirement accounts by April 1st of the year after you turn 72, and each year thereafter by December 31st.

- You can calculate your RMD by dividing your account balance as of December 31st of the year prior by your distribution factor which can be found on the IRS’s uniform lifetime table

- Check out our infographic below to see if you’re subject to an RMD this year

You are required to make your first required withdrawal from your retirement accounts by April 1st of the year after you turn 72. After that, you must make one every year by December 31st. This is known as Required Minimum Distributions or RMDs.

What is a Required Minimum Distribution (RMD and when do I need to take one?

Traditional retirement accounts like a 401(k), IRA, or 403(b) are typically tax-deferred. That means that you don’t pay taxes on the money you contribute and you don’t pay taxes on the money while it sits in the account and grows.

Tax deferral, however, means just that. It only delays them until you start withdrawing the funds from your account.

So if you don’t need the additional income, why not just wait to withdraw as long as possible? Well, Uncle Same won’t let you delay them indefinitely because they’re going to want their tax revenue.

That’s where RMDs come into play. Under current law, you are required to start making withdrawals from your retirement accounts by April 1st of the year after you turn 72.

It used to be 70 ½ before the SECURE Act.

By the way, if you like rules, you’ll like this handy RMD decision tree to help you determine if you need to make a required minimum distribution this year or not.

If you’re planning to wait until April 1st of the following year, keep in mind that you will be required to take TWO RMDs in that year.

For example, if you turned 72 in December of 2021, but decide to wait and take your RMD in 2022 by April 1st, that RMD will count towards your 2021 requirement and you will still need to take an RMD for 2022 by December 31st, 2022.

RMDs apply to all tax-deferred accounts which include:

- 401(k) plans

- 403(b) plans

- 457(b) plans

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- Profit-sharing plans

Roth IRAs are not subject to RMDs because the money was taxed before making a contribution to the account. Basically, Uncle Sam has no incentive to make you withdraw from a Roth IRA. That’s why you’ve probably heard of people rolling over their tax-deferred accounts into a Roth IRA, but we’ll touch on that more in a bit.

If you don’t need the income from your RMD to cover your retirement expenses, then an RMD may cause you more headaches. In addition to having to calculate them every year, they could result in excessive and unnecessary taxable income, and if you fail to withdraw the minimum amount, you’ll be facing a heft fine.

How to calculate your Required Minimum Distribution

Here is the formula to calculate your RMD:

You are required to use this calculation to determine your RMD for every retirement account you have that is subject to an RMD.

RMD Table for 2022

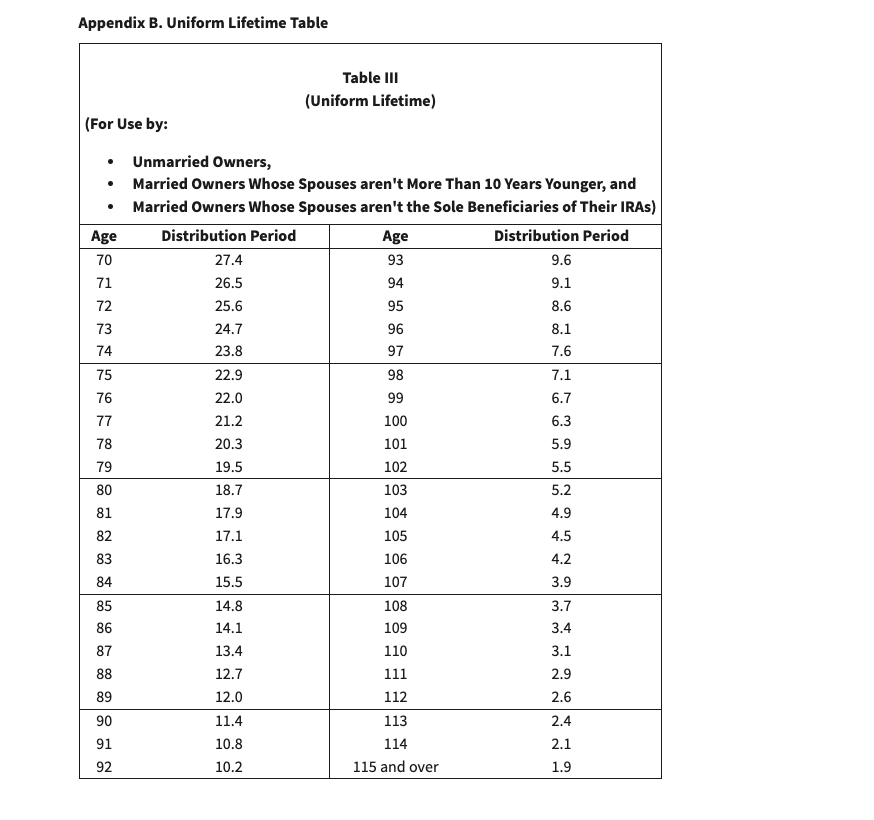

The IRS recently released new life expectancy tables for 2022. These tables are used to determine your RMD.

Quick note: If you’re making your first RMD by April 1st, 2022 because you turned 72 last year, you will need to use the previous RMD tables which I will link below.

There are two different sets of distribution factors (or RMD tables). If you’re single OR married and your spouse is not more than 10 years younger, you will use the uniform lifetime table.

If you are married AND your spouse is more than 10 years younger and the sole beneficiary on your account, then. you will need to use the joint-life & last survivor table.

I’m going to use the uniform lifetime table because it’s more widely used. If you have any questions regarding the joint-life & last survivor table we’d be happy to help.

After a gruesome deep-dive on Google, beyond the first page, and past the paid ads, I found a link to the updated uniform lifetime table for you. I also went ahead and put the table down below so you don’t have to scroll the 2 miles it takes to find it. Trust me, my fingers are still recovering.

Required Minimum Distribution (RMD) table for 2022

| Age of retiree | Distribution factor | Age of retiree | Distribution factor |

|---|---|---|---|

| 72 | 27.4 | 97 | 7.8 |

| 73 | 26.5 | 98 | 7.3 |

| 74 | 25.5 | 99 | 6.8 |

| 75 | 24.6 | 100 | 6.4 |

| 76 | 23.7 | 101 | 6.0 |

| 77 | 22.9 | 102 | 5.6 |

| 78 | 22.0 | 103 | 5.2 |

| 79 | 21.1 | 104 | 4.9 |

| 80 | 20.2 | 105 | 4.6 |

| 81 | 19.4 | 106 | 4.3 |

| 82 | 18.5 | 107 | 4.1 |

| 83 | 17.7 | 108 | 3.9 |

| 84 | 16.8 | 109 | 3.7 |

| 85 | 16.0 | 110 | 3.5 |

| 86 | 15.2 | 111 | 3.4 |

| 87 | 14.4 | 112 | 3.3 |

| 88 | 13.7 | 113 | 3.1 |

| 89 | 12.9 | 114 | 3.0 |

| 90 | 12.2 | 115 | 2.9 |

| 91 | 11.5 | 116 | 2.8 |

| 92 | 10.8 | 117 | 2.7 |

| 93 | 10.1 | 118 | 2.5 |

| 94 | 9.5 | 119 | 2.3 |

| 95 | 8.9 | 120 and older | 2.0 |

| 96 | 8.4 |

Here’s a link to the previous IRS uniform lifetime table as promised and to save you some PSFP (post-scroll finger pain), here’s a screenshot you can download.

So let’s look at an example: You just turned 75 and you have $150,000 in your IRA. Here’s what the calculation would look like.

If you have multiple retirement accounts, you will need to calculate each RMD separately for each account.

Don’t want to do the math by hand? Here’s an RMD calculator you can download.

How do RMDs work if I have multiple accounts?

As I mentioned above, if you have multiple retirement accounts, you will have to calculate the RMD for each account separately.

While you have to calculate each account’s RMD separately, in some cases, you can take the total RMD amount from one account. If you have separate IRA accounts, you can aggregate the total amount across accounts and take that amount from just one of your IRAs. This works with traditional, SEP, and SIMPLE IRAs.

For example, let’s say you have 3 IRAs and the RMD is $250 for each. You have the option to either take $250 from each account or take the total of $750 from one account or a combination.

However, RMD aggregation is not allowed across employer plans like 401(k)s and 403(b)s.

What if my spouse and I have separate retirement accounts? Can we combine our RMDs and take them from one account?

Short answer, no. If you’re married and have separate retirement accounts, you must take your RMDs separately from each other. Your RMDs cannot come solely from one spouse’s account.

What happens if I don’t take an RMD?

If you don’t take your RMD there is a penalty and a hefty one at that. I recommend setting an annual reminder just in case you don’t end up making a withdrawal or aren’t sure if you’ll meet the minimum requirement throughout the year.

The penalty for not making a required minimum distribution is 50% of the amount not taken on time.

For example, if your RMD is $500, but you only take $200, then you will owe Uncle Sam an additional fine of $150 (50% of the $300 you didn’t withdraw) in addition to the amount you still owe.

Make sure to follow the IRS guidelines and consult your tax advisor for more information.

Are RMDs taxable?

Yes, your RMD is considered part of your annual income. The total amount of your withdrawal (or RMD) is taxed as ordinary income based on your income tax rate.

You can also have the tax withheld from your distribution instead of waiting until the end of the year. Check with your retirement account custodian because they should have a form or online process when you request your distribution that will ask if you’d like to withhold any amount to be sent to the IRS.

You should also consult your tax advisor as they can put together some projections and give you a recommendation on how much to withhold.

Remember when I mentioned that you have until the following year of your 72nd birthday to take your first RMD? Let’s go back to that quickly since we’re talking about taxes.

If you take two RMDs your first year, it could push you into a higher tax bracket which would mean you’ll owe more in taxes that year. Depending on your circumstances, this could also make you subject to the Medicare high-income surcharge if your modified adjusted gross income is over $91,000 if you’re single or $182,000 if you’re married and filing jointly. And if you receive Social Security, a larger portion could be subject to taxation.

At the risk of sounding like a broken record, reach out to your financial advisor and tax accountant BEFORE you turn 72 so they can help you determine the best plan of action based on your particular circumstance.

It’s important to stay ahead of taxes when it comes to retirement. The sooner you start planning the better and here’s why…

RMD Creep

No, I’m not talking about the IRS coming after you for their tax money. I want to talk about why you should think about managing your RMD BEFORE you hit 72 years old. Like way before.

There’s this thing called the “RMD Creep” and what I mean by this is that when you first turn 72 years old, your required minimum distribution will start out relatively small, but as you get older your RMD will likely grow exponentially. There are two factors that are at play here:

- As you age, the amount you’re required to withdraw also increases

- And depending on your portfolio, the investments in your retirement accounts can continue to grow

The most common mistake is that retirees will only look at their RMD in the first few years of the requirement and think that it will remain steady. However, the distribution factor changes as you get older. The older you get, the lower your distribution factor is which will increase your required minimum distribution.

A higher RMD may force you into a higher tax bracket throughout retirement which can cost more than most retirees plan for. You can avoid some of these tax hits if you plan ahead and address these issues earlier on in retirement. That’s why it’s crucial to develop a tax strategy with your financial advisor and tax accountant in order to avoid costly tax surprises down the road.

Here are 5 ways to use or minimize your Required Minimum Distributions

1. Manage Your Withdrawals before 72

When you turn 59 ½, you can start making withdrawals from your retirement accounts without a penalty. They are still taxed as regular income, but if you work with your financial advisor or accountant, they can help you figure out how much you can withdraw without moving into a higher tax bracket.

Over time, the withdrawals will reduce the amount in your tax-deferred accounts which will result in a lower RMD when you reach 72.

2. Convert funds from your Traditional IRAs and 401(k)s to a Roth IRA before 72

But once your money is in a Roth IRA, it can grow tax-free and withdrawals are nontaxable throughout the rest of your retirement. They also don’t come with required minimum distributions at age 72.

3. Reinvest it

If you don’t have an option to reduce or avoid your RMD and you don’t need it to cover expenses, you can always reinvest it into a taxable brokerage account.

If you make a conversion to a Roth IRA, you can reduce your RMD. If you do it before you turn 72, you can potentially eliminate your RMD requirement completely. Keep in mind, that the amount you convert from your tax-deferred account to a Roth IRA will be treated as income and taxed as such. This may cause your tax bracket for the year to increase.

4. Give it to Charity

Once you hit RMD age you can give up to $100,000 from your IRAs to an eligible charity, tax-free, every year. This is called Qualified Charitable Distributions (QCDs). A QCD isn’t taxable and will count towards satisfying your RMD for the year as long as the organization is considered qualified by the IRS.

As long as the organization is qualified, you can have your RMD check issued directly to them.

There are two rules when making a QCD:

- The transfer must be made to the charity directly from your IRA in order for it to not be included in your adjusted gross income.

- You can’t claim the donation as a charitable deduction on your annual taxes.

You can use the IRS’s tool to see if a charity is qualified. Keep in mind, that this is only eligible for IRAs.

5. Keep working

If you continue to work past the age of 72 and you don’t own 5% or more of the company, you can avoid taking RMDs from the retirement account sponsored by your current employer until you retire.

Here’s the caveat, this only applies to your 401(k) at the company you’re working at. If you have another 401(k) or IRA from a previous employer, you’ll need to make an RMD on those accounts. Want a caveat to the caveat? If your current employer allows rollovers, you can transfer a 401(k) from a previous employer into your current account. This does not work with IRAs though.

Don’t Forget

No matter when you decide to take your required minimum distribution and how you’re going to use it – consulting your financial advisor and tax accountant well before the age of 72 will give you the best options based on your situation. Also, remember to take it by December 31st (please set a reminder!) so Uncle Sam doesn’t get half of what you should have withdrawn.

Here at Odyssey, we’re always available to help if you have any questions. You can reach out to one of our retirement consultants here.

About The Author Stephanie joined the Odyssey Advisor’s team all the way from the Lonestar state in November of 2020. She is versatile in her abilities and has experience in copywriting, photography, and analytics. She helps tell our brand story and convey...

More Insights From This author

{kind=link}