Why Your OPEB Costs May Be Higher Than You Think

Bottom Line Up Front

- Early retirement can significantly increase your OPEB liability by extending the years of employer-covered healthcare.

- Spousal coverage, especially for younger spouses, can more than double your financial obligation.

- Transferred service and flexible spousal enrollment rules can leave your organization footing the bill for benefits earned elsewhere or added late.

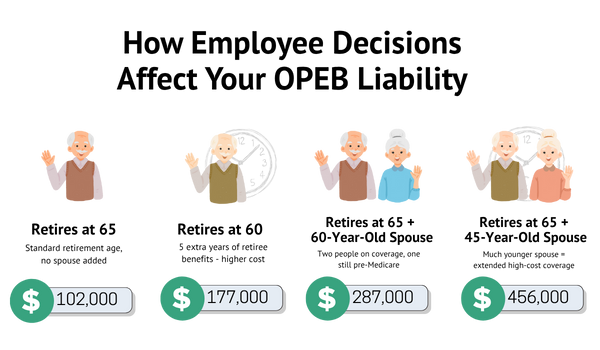

Meet John. John joined your organization at age 25 and stayed through his entire career. He’s reliable, dedicated, and the kind of employee any employer would be lucky to have. Now, at age 65, John is ready to retire.

If John retires at 65 and takes retiree healthcare coverage, the total present value liability* to your organization is about $102,000.

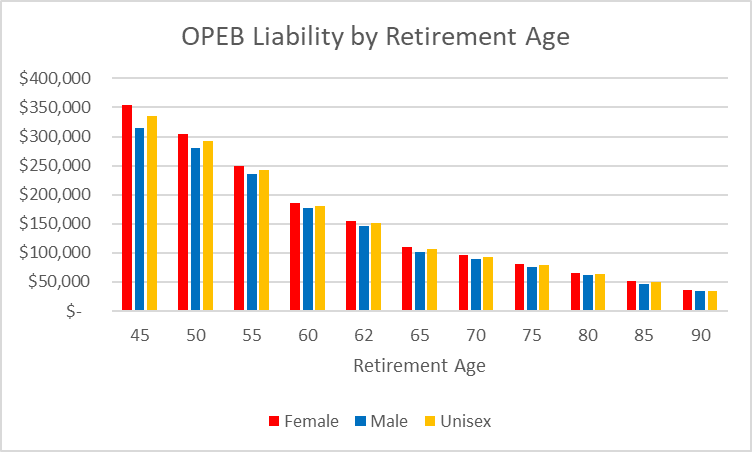

To help illustrate how OPEB liability can change based on key decisions, we’ve included a table below that shows expected present value liabilities for both males and females at various retirement ages. These figures will serve as the foundation for the scenarios we’ll explore.

But what if John retires earlier? What if he decides to cover a spouse? Or what if that spouse is significantly younger than him? Each of these decisions could substantially increase your organization’s Other Post-Employment Benefits (OPEB) liability.

Let’s follow John through a few different retirement scenarios to better understand how OPEB costs can quickly add up.

OPEB Liability by Retirement Age

| Retirement Age | Female | Male | Unisex |

| 45 | 354,000 | 315,000 | 335,000 |

| 50 | 305,000 | 281,000 | 293,000 |

| 55 | 249,000 | 233,000 | 242,000 |

| 60 | 185,000 | 177,000 | 181,000 |

| 62 | 155,000 | 147,000 | 151,000 |

| 65 | 110,000 | 102,000 | 106,000 |

| 70 | 97,000 | 89,000 | 93,000 |

Disclosures/Assumptions

- Discount Rate: 4.00%

- Medical Care Cost Inflation Rate: Getzen Model of Long-Run Medical Cost Trends for Active and Medicare Supplement Plans

- Average pre-65 premium: $955.80

- Post-65 premium: $443.40

- Mortality: RP-2014 Mortality Table for Blue Collar Employees projected generationally with scale MP-2021, set forward 1 year for females

- Cost Sharing: Employer pays 20% of premiums

- Liability: Represents the present value of all future payments as of the date utilizing the discount rate, mortality rate, healthcare inflation, and insurance costs above.

*OPEB liability estimates are based on standardized assumptions, including a 4.00% discount rate, projected healthcare inflation, and average premium costs. Figures are for illustrative purposes only and may not reflect your plan’s actual design or funding approach. For a personalized valuation, please consult a qualified actuary.

How do Benefits Change with Early Retirement?

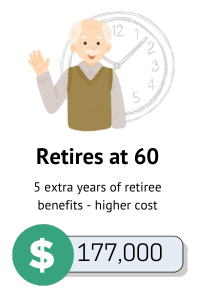

Let’s say John retires at 60 instead of 65. At first, it may not seem like a big change. It’s only a five year difference.

But now, your liability jumps to $177,000, an increase of $75,000.

Why? You’re now covering five extra years of retiree healthcare. John will stay on the Active healthcare plan until age 65, which tends to be more expensive than Medicare-based coverage. Bottom line: the earlier John retires, the more expensive his benefit becomes.

What If The Employee Has Transferable Retirement Service?

Now, imagine John spent 35 years at another public organization in the same retirement system. At age 60, he joins your organization and retires at age 65. Even though he only worked with you for five years, your organization inherits the full $102,000 OPEB liability.

That’s because some systems allow for transferable service credit, and the liability is borne entirely by the last employer unless there is a policy in place to share liability based on service or some other metric.

In this case, you had only five years to fund a benefit that normally accrues over 40 years.

⚠️ Be aware of your retirement system’s eligibility rules; transferred service can cause unexpected financial strain.

What Happens When a Retiree Covers Their Spouse?

Let’s return to the first scenario: John retires at 65. If he elects to cover his 60-year-old spouse, your liability doesn’t just increase; it nearly triples.

- John’s solo liability: $102,000

- With spouse: $287,000

That’s an increase of $185,000.

Why such a big jump? You’re covering two people now, not just one. The spouse is under 65, so she’ll be on the Active plan until eligible for Medicare, just like John was in the early retirement example.

How Does a Much Younger Spouse Affect The Liability?

Here’s where it gets even trickier.

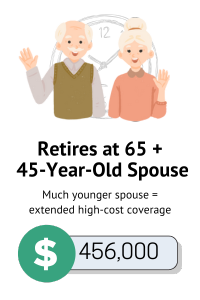

Let’s say your plan allows retirees to add a spouse at any time. John retires at 65, then marries a 45-year-old woman and adds her to his retiree coverage.

Your new OPEB liability? $456,000. That’s an increase of $345,000 from when John was retiring alone (if they have children, those costs are even higher).

While rare, these scenarios do happen, and they underscore the importance of plan design. Consider limiting spousal eligibility to those covered at the time of retirement to avoid surprises.

Understanding the Biggest Drivers of OPEB Liability

John’s story illustrates a few key truths:

- Retirement age matters – early retirements result in higher costs.

- Spousal coverage matters – covering a spouse, especially a younger one, can more than double liabilities.

- Eligibility rules matter – transferred service and flexible spousal enrollment can burden your organization with significant, unexpected costs.

That’s why it’s essential to have an actuary perform an OPEB valuation at least once every two years. Actuaries use data-driven assumptions, like retirement age and spousal election probabilities, to calculate service cost, the annual cost of benefits earned.

By funding that amount each year, your organization stays ahead of the curve, avoids budget surprises, and ensures long-term sustainability.

While employee decisions may not always align with assumptions, pre-funding your OPEB plan is your best strategy for minimizing financial strain.

At Odyssey Advisors, we work with municipalities and public sector organizations across the country to plan, manage, and fund their OPEB obligations. Have questions? You can reach one of our actuaries or actuary consultants here.

About The Author Luke graduated from the University of Connecticut with a B.A. in Actuarial Science. He brings a strong mathematical and analytical background to his role as a Consulting Actuary at Odyssey Advisors. He designs and maintains complex client-employee benefit programs...

More Insights From This author

Explore More Resources