FSA vs HSA vs HRA: Which One is Better?

KEY POINTS

- The 3 most popular employer-sponsored healthcare accounts you can supplement your current healthcare insurance with are Flexible Spending Accounts (FSA), Health Savings Accounts (HSA), and Health Reimbursement Accounts (HRA).

- FSAs, HSAs, and HRAs all offer tax-free savings that you can use to pay for eligible medical, dental, vision, and sometimes long-term care expenses.

- The bottom of this article includes an in-depth table comparing the three accounts.

Good healthcare insurance is an important benefit that many employees look for. In addition to insurance, many employers offer supplemental plan options. In this article, I’m going to cover the key differences between the 3 most popular employer-sponsored accounts: Flexible Spending Accounts (FSA), Health Savings Accounts (HSA), and Health Reimbursement Accounts (HRA).

Flexible Spending Account (FSA)

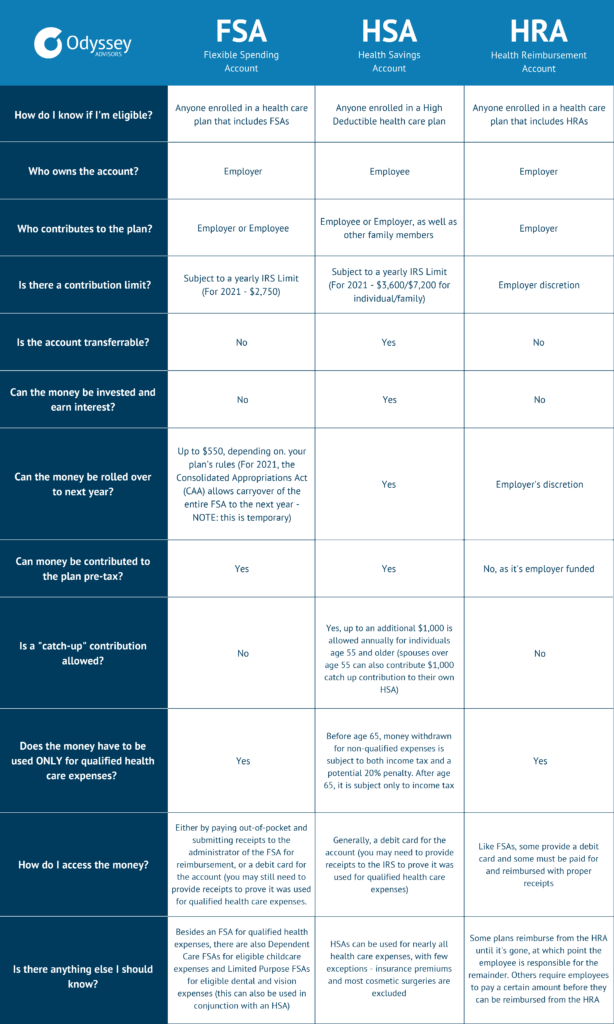

FSAs are employer-owned, but employee-funded accounts that can be used to pay for any eligible healthcare costs that aren’t covered by your healthcare insurance. They’re available to anyone with a healthcare plan that includes them. You can make contributions to the account pre-tax (subject to a yearly IRS limit), but you can only rollover $550 to the next year. You’ve probably seen the advertisements at the end of the year reminding people to use their FSA funds before they expire. Upon termination of employment, any unused funds left in your FSA will most likely be forfeited back to the employer.

Health Savings Account (HSA)

HSAs are for anyone that has a qualifying high deductible plan (for 2022, an HDHP has an annual deductible of at least $1,400 for single and $2,800 for family coverage). Like FSAs, contributions can be made pre-tax. Unlike FSAs, however, the account belongs to you and can be transferred to your next job. Additionally, funds do not expire at the end of the year and can even be invested within the account. If funds are withdrawn for non-qualifying expenses, they’re subject to income tax (as well as an additional 20% penalty if you are under the age of 65).

Health Reimbursement Account (HRA)

HRAs are not owned by the employee, nor does the employer contribute to the plan — which means no portability when your employment is terminated. HRAs can be used in conjunction with both FSAs and HSAs. When paired with an HSA, the HRA can only be used for either dental or vision benefits or strictly for amounts over your deductible. After age 65, HRA contributions can be used to pay premiums (health, dental, vision, and long-term care) for the primary participant.

FSA vs HSA vs HRA Comparison Table

Many factors determine what health plan is right for you and what supplemental plans might be most beneficial. When comparing FSA vs HSA, HRA vs HSA, or FSA vs HRA, it’s important to consider each plan with your particular circumstances. If you’re thinking about adding an FSA, HRA, or HSA plan to your health insurance, you can talk with your insurance provider or reach out to one of our Odyssey Consultants to determine if any of these might be a good fit for you and your specific needs.

Interested in learning more?

About The Author Before coming to Odyssey Advisors, Samantha spent 8 years as a high school math teacher, working mostly with students in low-income, at-risk communities. She users her education background to make sure clients understand the often complex world of retirement benefits...

More Insights From This author