What is Medicare Advantage?

Wading through all of the insurance plans out there can be overwhelming. Have you seen the Joe Namath commercials yet where he hypes up all the benefits of Medicare Advantage? With so many options, Medicare Advantage is a phrase you hear more often than the rest. Mainly because of how it’s funded.

What is Medicare Advantage?

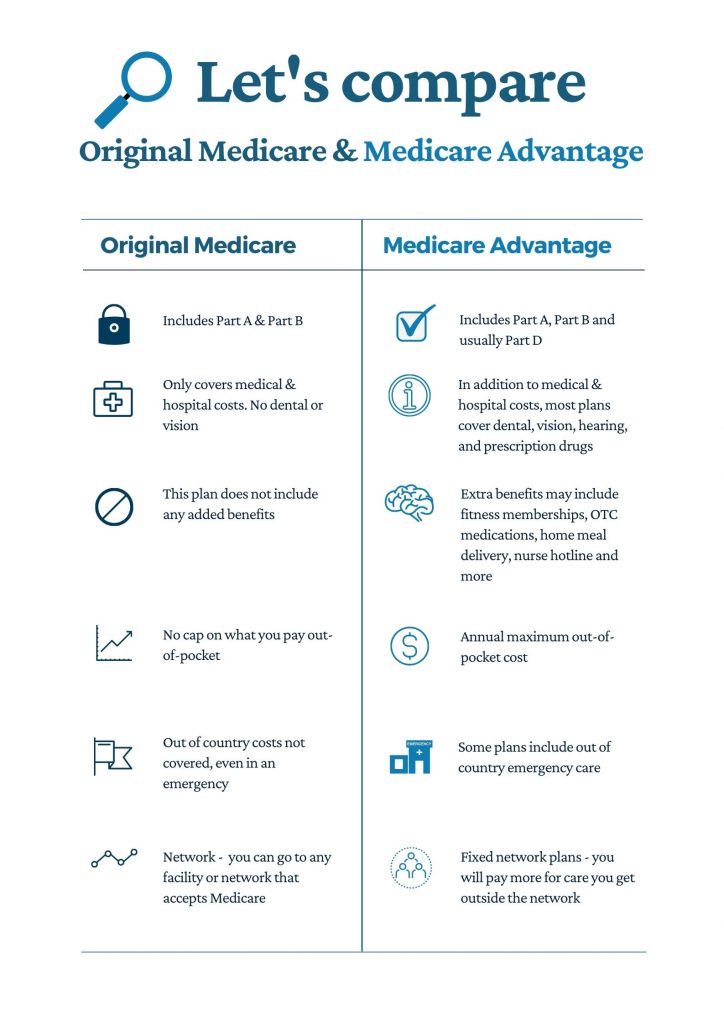

Medicare Advantage plans, also known as Part C, are offered by private insurance companies that have contracts with Medicare. Advantage plans allow you to receive Part A, Part B, and Part D benefits all in one unlike the Original Medicare.

How Medicare Advantage Plans work

Each plan varies, but the insurance company pays out instead of Medicare. Medicare pays a fixed monthly amount to the issuer of the Medicare Advantage plan. In return, the issuer must offer at least the same benefits as Medicare Part A, hospital, and Medicare Part B, medical coverage.

Additional services and benefits offered vary by issuer. Some Advantage plans are either HMOs or PPOs with different networks. Some may have different out-of-pocket costs. And there are some that have different regulations on how you receive services. For example, if you need to see a specialist, you may have to go through your primary care physician to request a referral first.

Medicare Advantage plan costs

Medicare Advantage plan premiums vary based on the benefits. They can be as low as $0. To qualify for Medicare Advantage, you must be enrolled in Parts A and B which means you will be responsible for any applicable premiums.

If the you worked and paid Medicare taxes, you will most likely receive Part A premium free. Part B has a premium and a deductible. Costs for Part B are based on your lifetime earnings.

Benefits

- Annual out-of-pocket maximum

- More coverage than Original Medicare

- May have coverage while abroad

- Fixed copays mean you are better able to anticipate costs and they may be lower than coinsurance

- Provides multiple types of coverage all in one plan

- Coordinated care – your healthcare providers actively communicate to coordinate your care which may avoid unnecessary expenses and adverse medication interactions

- Ability to choose plans that best meet your needs (e.g. there are plans tailored to patients with chronic conditions)

Drawbacks

- Limited network

- Certain services may require a referral or special authorization

- Networks are regional – you may find it difficult to receive services outside your region

- The out-of-pocket maximums can be quite high

- The benefits that different Advantage plans offer can be complex and difficult to understand

- There may be fees that Original Medicare plans don’t have such as drug deductibles

Key takeaways

Advantage plans offer benefits that Original Medicare doesn’t, which if needed, can save you money. It’s important to weigh the pros and cons when selecting coverage. Even though Advantage plans have a maximum for out-of-pocket costs, the cap can still be high. And in order to receive these additional services, participants give up the flexibility that Original Medicare offers.

If you are a municipality looking to learn more about how to manage your OPEB liability, this plan is a private-sector alternative or replacement for Medicare which can often provide equal or better benefits for the same cost or less. Interested in how you can manage or even reduce your town’s OPEB liability? You can reach out to one of our Odyssey Advisors for a free consultation.

Categories: OPEB

About The Author Sarah has a Bachelor of Science in Mathematics from the State University of New York at Brockport and is a Member of the American Academy of Actuaries and an Associate in the Society of Actuaries....

More Insights From This author